EU to Render Permanent the 'Temporary' Emergency Due to (drum roll) Russia! Russia! Russia!

'Measures are…maintained as long as the making available of…resources to Russia…poses, or threatens to pose, serious economic difficulties within the Union'.

Every now and then, we need to revisit ‘old’ pieces to figure out how far off my musings were. Today is such a day, and we’ll be talking about the EU and the Commission’s desire to become ‘more’.

This is ever more pertinent as the EU Commission, on 7 Oct. 2024, released a news item announcing their creation of a what is called a ‘repo facility’.

Commission launches EU Repurchase Agreement, thereby becoming a sovereign-style issuer on EU capital markets.

That is, it shall be noted, the EU Commission’s language. From my piece (linked below):

It might not come as a surprise to you, but the EU Commission is arrogating the privileges (no constitutions, no laws or rights) of ‘a sovereign-style issuer’.

In the US context, it took both the Federal Reserve Act of 1913 and the US entering the First World War before such repo arrangements were used from 1917 onwards…

The EU Commission has just declared its de facto sovereign authority…

The first EU repo transactions will be executed today on the Eurex Repo web-based trading system and will be cleared via Eurex Clearing.

Repo facilities are commonly used by sovereign issuers to support the market activity of their primary dealers [they are, in other words, a massive gov’t intervention that favours one kind of market (sic) participants—the EU ‘primary dealers’—over everybody else]. The EU Repo facility operates in line with standard practices of peer sovereign issuers [hence the importance of esp. what the US Federal Reserve does]. The launch of the Repo facility marks the implementation of the final measure announced by the Commission in December 2022 to support the EU bonds market. The Commission has now all the tools that it needs to manage successfully a busy period of issuance to end-2026 with the support of its valued Primary Dealer Network.

Read the rest here:

Why Does This Matter Re: ‘the frozen Russian assets’?

This is supremely important as the depository in question—Belgium-based Euroclear—holds gargantuan amounts of assets worldwide; Russia has already initiated legal proceedings under the otherwise problematic ‘investor state dispute settlement’ (ISDS) procedures, which were roundly denounced as the most insidious parts of both Obame-era ‘trade agreements’ TTIP and the TTP.

In other words: the proceedings currently ongoing are taking place in a parallel arbitration system otherwise unavailable to John and Jane Q. Public.

The best write-up (dated 12 Dec. 2025) I’ve yet seen is by Yves Smith over at nakedcapitalism.com (link).

This issue are discussed™ by the Foreign Affairs EU Council—the foreign ministers of all EU member-states—on 15 December 2025 (see their agenda) before this is formalised™ by the heads of gov’ts in their EU Council meeting on 18-19 Dec.

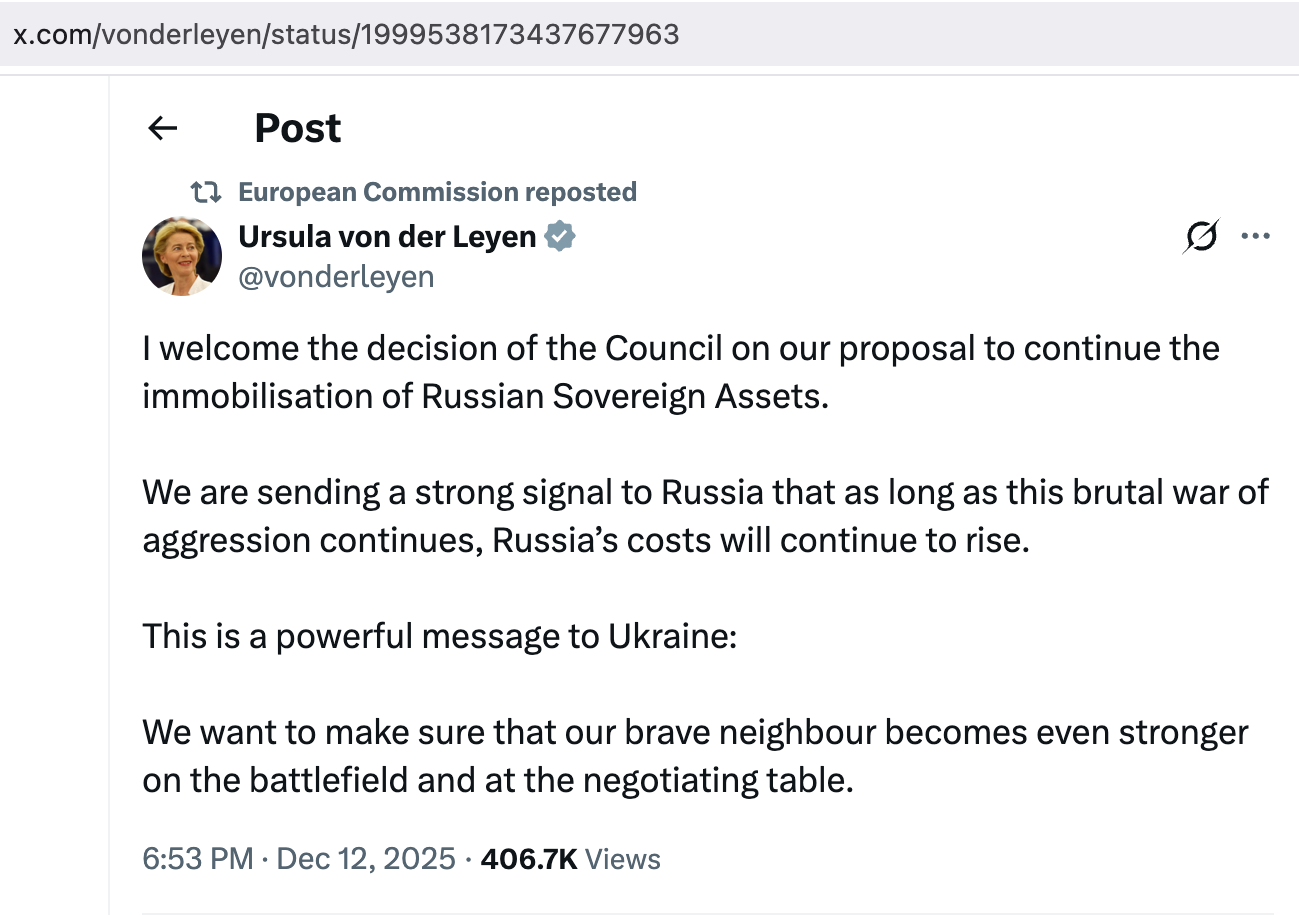

Yet, the significance of these ‘frozen Russian assets’ transcends the immediacy of these shenanigans—for here’s the true issue behind this (sooper-dooper stupid) move as ‘splained in a formal EU press release dated 12 Dec. 2025 (Italics in the original, emphases mine):

Council decides to prohibit transfers of immobilised Central Bank of Russia assets back to Russia

The Council today decided to prohibit, on a temporary basis, any transfers of Central Bank of Russia assets immobilised in the EU back to Russia. This decision was taken as a matter of urgency to limit damage to the Union’s economy…[here follows some boilerplate virtue-signalling I’ve omitted]

The measures are temporary and should be maintained as long as the making available of significant financial and other resources to Russia to continue its actions in the context of its war of aggression against Ukraine poses, or threatens to pose, serious economic difficulties within the Union and the member states and the risk of causing further serious deterioration of the economic situation in the Union and in the member states persists.

These highlighted, if truncated, parts of the last paragraph are literally the money shot by the EU leadership caste.

Whatever they say this is about, please re-read carefully what they mean:

Measures are…maintained as long as the making available of…resources to Russia…poses, or threatens to pose, serious economic difficulties within the Union

This is nothing short than the declaration of a state of emergency that arrogates further power to Brussels, and this is done ‘as long as’ whatever ‘threat’ that is invoked ‘threatens to pose’ consequences.

This isn’t merely totally elastic in terms of anything tangible and/or concrete; it’s falling far, far short of a legislative™ act, even in the less-than-constitutional ways and means (ahem) this means in the context of the EU leadership caste.

(For background on how the EU was set up and how to understand its functioning™, please refer to this piece:

And now back to the main course.)

Here’s a totally obvious parallel, by the way:

This press release is nothing but a power grab by the EU Commission whose main players seek to obtain tyrannical powers that exceeds anything seen in Central Europe since 1945.

This is an extraordinary claim, I know, and I don’t make it lightly. Yet, I am quite convinced that this declaration of intent affords such an incredible amount of executive authority to a single, unelected non-governmental institution (the EU Commission), that this categorisation is valid and, in fact, warranted.

Remember, the EU Commission declared that they get to decide

as long as the making available of…resources to Russia…poses, or threatens to pose, serious economic difficulties within the Union

The EU Commission arrogates to itself that kind of emergency authority, which it will maintain until further notice (by itself).

Carl Schmitt once quipped: ‘sovereign is he who decides on the exception’, and we all know who did that.

This is both another clear breach of the EU Treaties (which, technically speaking, the EU Commission is tasked to ‘guard’ and ‘uphold’) and, given the sordid history of the past 5+ years, nothing new.

Let us, then, compare this statement with the good ol’ days when tyranny required at least a law formally passed by a parliament, such as Enabling Act of 1933 (hence EA), which legally cemented into place Hitler’s dictatorship in Germany?

Well, for starters, the 1933 law a tad longer and more comprehensive, for it stressed (EA §1) that ‘laws of the Reich may also be enacted by the government’, hinting at jurisdictional clarification. The above-related decision explicitly affords the authority to do whatever is necessary in these manners, i.e., it there is no need to actually bother the parliaments or governments of any of member-states before this decision is formalised in the Foreign Affairs Council on 15 Dec.

EA §2 similarly grants broad and unchecked powers to the government, holding that ‘laws enacted by the government of the Reich may deviate from the constitution as long as they do not affect the institutions of the Reichstag and the Reichsrat’. Here, I shall point the reader to the single sentence quoted above, which afford the EU Commission the authority to decree any changes unless the ‘threat’ is no longer ‘posed’. There is nothing in this statement of intent that reeks of evidence-based decision-making, parliamentary or judiciary oversight, or any sunset clause written down.

It’s all make-believe, said and done.

In this context, I shall argue that doing so is consistent with my hypothesis of a ‘technocratic’ caretaker government take-over to prevent any accountability, oversight, or the possibility of the peoples of the member-states having any say in these matters masquerading as a politicking as usual.

There’s nothing normal about this, and that’s perhaps the point.

Bottom Lines

On closer inspection, there is another aspect that begs consideration:

As Ms. Von der Leyen was quick to point out, this is a kind of Sicilian message (via ‘The Godfather’), and I’m certain that the proximal addressee isn’t Russia! Russia! Russia! as much as it is all the other EU member-states:

Cross the EU Commission, and they’ll immobilise their assets claiming that, say, Viktor Orbán’s Hungary or Robert Fico’s Slovakia

poses, or threatens to pose, serious economic difficulties within the Union

And there you go.

If you’re still harbouring doubts about the true measure of this shitty decision by the EU Council, here’s some food for thought from Valérie Urbain, Chief Executive Officer of Euroclear, who commented:

Our performance demonstrates the continued strength and resilience of our business. We delivered solid growth in our core activities, with underlying business income up 7% year-on-year to €1.4 billion and our operating margin improving to 27.4%. In the nine first months of 2025, our systems seamlessly processed 267 million transactions worth over €1 quadrillion. This represents a year-on-year increase of 20% and a new record confirming Euroclear’s systemic role at the heart of the global capital markets [be afraid, be very afraid,

ifwhen anything goes wrong].In Europe, we continue to implement our vision for a true Savings and Investments Union – one that delivers tangible benefits to issuers, investors and all users through deepening liquidity pools, ensuring systems are interoperable and asset classes are fungible. Euroclear’s plan is clear: providing a single [huhum, what

couldwill go wrong?] point of access [give me a lever, and I’ll move mountains, if not mountain ranges of debt] across all financial asset classes [Euroclear is The One Ring to Bind Them All] to the 27 Member States and the UK [oh, hi there, Brexiteers-in-name-only, how’s that going for you?]. This commitment is supported by innovative projects to develop a modern and interconnected market infrastructure, most recently illustrated by our collaboration with Banque de France to tokenise short-term debt Negotiable European Commercial Paper (NEU CP) [that would be, in their own words, ‘The Paris-based Negotiable EUropean Commercial Paper (NEU CP) market is the leading short-term debt market in the European Union. It plays a key role in financing the economy.’ See also this Bloomberg piece and the footnote for relevant quotes1] on our DLT platform.We are aware that the European Commission is working on a proposal to provide Ukraine with a Reparations Loan. We expect to receive further information on the envisaged mechanism and will continue to engage with decision-makers. Any proposal should respect international law and internationally accepted legal principles underpinning Western economies and protect the interests of Euroclear and its stakeholders.

That last sentence is a yuuuuuuge middle finger directed at the EU Commission.

Over the weekend, Slovakia and Italy have joined Euroclear and Belgium in their ‘reluctance’ to trigger this bomb.

I personally consider it too little, too late, with the runway ending, formally speaking, on 18-19 Dec. 2025 in that EU Council meeting in Brussels.

I suppose it’s not too far-fetched to consider an extended bank holiday over the Christmas holidays as a plausible way forward.

Don’t forget to stock up on a bit of extra food, cash, and other things you might need, in particular if you have pets before Christmas. Consider board games and physically existing books as (extra) presents, for they may come in handy before too long.

And let’s just note a few preliminary signs, with date stamps included:

All is going according to Our Beloved Central Planners (December is also o.k.):

I’ll leave you with this gem of a receipt:

The Great Sorting is Here

Oh my, now we must talk about the future of the occupation régime known as ‘the European Union’ once more—due to big news coming out of Warsaw, Poland:

Stay frosty, and whatever you do, don’t panic and do not be afraid.

In case you, perhaps being based outside the mental asylum masquerading as the EUropean Union, thought that whatever TF happens with the loonies in Brussels might stay in Brussels, here’s the key take-away from that Bloomberg piece:

Isabelle Delorme, Head of Product Strategy and Innovation at Euroclear, said: ‘Collaborating with Bloomberg allows us to strengthen the largest commercial paper market in the euro area through an open and same-day issuance framework. This contributes to a more efficient, standardized and streamlined issuance ecosystem, reducing market fragmentation and boosting liquidity. This step further cements Euroclear’s position as a vital financial market infrastructure, connecting issuers and investors.’

Please allow me to translate from the EUrocratese: whatever TF happens in Brussels will definitely not stay there; to the contrary, it will spread on the very same day.

Brad Foster, Global Head of Fixed Income Product at Bloomberg, said: ‘Our joint efforts with Euroclear to provide ISINs for our clients represents a logical next step on the path toward increased automation and transparency across money markets. We are committed to developing additional strategic collaborations and expanding our coverage and quality in money markets as we look for new ways to unlock value for our clients in fixed income.’

More translated content: whatever TF happens in Brussels will be automatically relayed = spread ‘across money markets’.

Oh, lest I forget, it’s the Banque de France that oversees™ and regulates™ this Negotiable EUropean Commercial Paper (NEU CP) market.

You’re welcome. Have a grandiose day.

This type of rhetoric usually precedes a wholesale collapse. It does not create confidence at all.

Those people... they have no understanding of things.

Think of a cottage. It is small and modest enough that one person can deal with most things in it and about it, and so that person understands all the needs and musts.

A mansion needs more than one and they need hierarchy and structure, but also autonomy: just as it is too large for one to handle, so too is the administration of every detail too much and so everyone working in the mansion needs autonomy to do their job right.

That same principle holds true for the EU, but the bosses here do the opposite: no autonomy, and just follow checklists to CYA, for all the servants and serfs.