Die Zeit Normalises Germany's and the EU's Gas Follies

'Everyone in the industry is now praying for warm weather.' ∽ An expert™, who knows the German gas market like no other, who is, of course, 'not considered an alarmist'

Just as the sheer scale of Germany’s most recent policy failure is breaking through on a technical level, legacy media is now reporting™ on the true state of affairs: we’re close to the end game, it would seem.

The below piece is quite telling, and I’m offering it in my translation, with emphases and [snark] added.

You might also be interested in where a sizeable part of German/the EU’s natural gas comes from (Norway), whose production of natural gas peaked in 2024:

And remember: what cannot be sustained, won’t over time.

Now the Only Thing That Helps is—Warm Weather

Germany’s gas storage facilities are rapidly emptying. Economics Minister Katherina Reiche is calm, but is even having a strategic reserve examined.

By Marlies Uken, Die Zeit [!!!] 17 Feb. 2026 [source; archived]

The expert, who knows the German gas market like no other, does not want to be quoted or recognised in any way. And he is not considered an alarmist either. But he says:

Everyone in the industry is now praying for warm weather. [I doubt anyone who is willing to see reality for what it is understands what this means: the risk of war is receding, for now, due to

bad weather energyconstraints; the risk of war™, however, is multiplying like rabbits in cornucopia, if only because this is the worst possible position for Germany to be in: unlike in the 1910s and 1930s, there’s not an inch of agency left for Berlin]

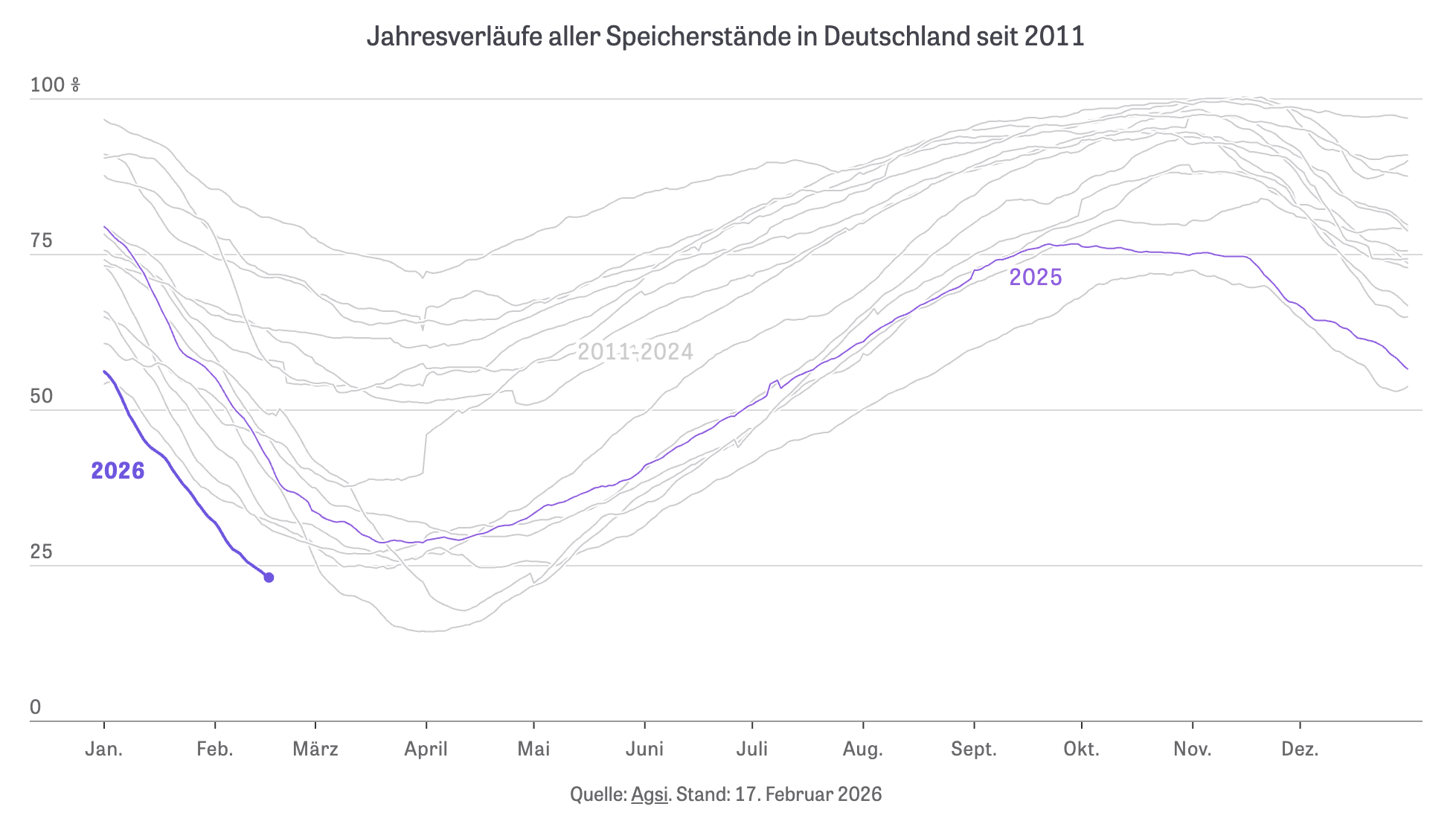

Anyone who takes a look at Germany’s gas storage levels can understand why.

[caption: annual gas inventory levels in Germany since 2011, with light purple = 2025—and the dark purple line indicating, well the present (2026)]

As Germany continues to shiver through the winter, gas storage levels are falling every day. Gas inventory levels stand currently only 24 per cent on average, Bavaria only manages to reach just under 18 per cent. The south is particularly affected because there are not that many storage facilities there, but there is a lot of industry that requires a lot of gas [below 20% inventory, it becomes hideously expensive to remove the gas from storage sites, by the way].

Officials—whether from the operators [who are notionally private™ actors], the federal government, or the Federal Network Agency—classify the situation as challenging but manageable. Only at the beginning of the month did Klaus Müller, head of the Federal Network Agency, reiterate his assessment that the gas supply was stable. When asked by Die Zeit on Monday [16 Feb. 2026], the Ministry of Economic Affairs informed Die Zeit that ‘the security of supply [orig. Versorgungssicherheit] in Bavaria, Germany and our neighbouring countries is not at risk’. Nevertheless, the members of the Economic Committee are questioning Economics Minister Katherina Reiche (CDU) and the head of the Federal Network Agency, Klaus Müller, this Tuesday evening. The issue, of course: the low inventory levels.

Headed Into Winter With Poorly Filled Storage Tanks

Germany started this winter with noticeably low filling levels—also because the storage operators had lost their business model. Until now, this was based on fluctuations: gas was fed in at low prices in the summer and sold at high prices in the winter. However, because there are now large quantities of liquid gas on the market worldwide, the price effect has been reversed. Gas sometimes costs more in summer than in winter—businesses collapses [note, for the record, that if your business is dependent on gov’t contracts, you’re not a free agent (here’s looking at you, Peter Thiel, Elon Musk, et al.]. Especially since the storage operators are betting that, in an emergency, the Ministry of Economic Affairs will commission the company Trading Hub Europe (THE) to fill the storage facilities with gas purchases [at any price] in accordance with the legal filling requirements [meant is a certain inventory level by a predefined date, which is what the gov’t-EU-cabal mandated in the wake of the Nord Stream bombings; in case you were still on the side-lines regarding the ‘more gov’t = good’ mantra—Germany’s energy woes are precisely the FAFO moment that was totally expected by everyone with more than one working brain cell at room temperature (proof: I wrote about this in Sept. 2021)] THE manages the gas market for the whole of Germany and ensures that there is always enough gas in the pipeline network. ‘Price signals on the gas wholesale market were distorted by the fill level specifications for gas storage’, says Sebastian Heinermann from the Ines storage association. A few days ago THE even put out a special tender so that the gas market can remain in balance in an emergency [nothing says ‘people are running around with their hair on fire while pretending, as hard as they can, that all is a-o.k.’ than the EU-tasked regulator/sooper-dooper agency offering a ‘special tender’, which is EU lingo for ‘we buy at this price’: hey, you brainiacs, what to you think the suppliers will do now? Exactly: wait a few more days before you up the ante…]

Storing gas is so unattractive that last fall the gas trader Uniper even applied to the Federal Network Agency to shut down a storage facility in Bavaria [remember: Uniper is a state-owned company™, which, is in cahoots (drum roll) with the Berlin gov’t: nothing says ‘I’m from the gov’t, and I’m here to screw you over’ like this absurdity; if this wasn’t Russian roulette (pun intended) with millions on the line, it would almost be hilariously funny as in: you cannot make this stupid shit up]. The market is now so dysfunctional that operators even preferred to sell gas directly from their storage facilities when gas prices rose this January because the weather forecasts predicted even more cold weather for Germany. Then filling levels fell even faster. The lower they are, the more technically difficult it becomes to withdraw the gas when necessary, as the industry says.

The government remains aggressively calm [i.e., they don’t do a thing; it’s a common feature among prey in nature, by the way]. They never tire of pointing to the four new liquefied gas terminals in Bremerhaven, Stade, Brunsbüttel, and Mukran on Rügen, through which Germany imports liquefied gas, in addition to the quantities that come via pipeline from Norway. However, these terminals can hardly increase their capacities—and their share of imports is only around ten per cent. The import level at German LNG terminals could still be increased by around 0.4 terawatt hours per day—but at temperatures around zero degrees Celsius, Germany consumes ten times as much. ‘It is far from enough to rely solely on the LNG terminals’, says Heinermann.

New Dependence on the USA

Especially since the situation is anything but stable, as the situation off Rügen shows: because of the cold and a thick layer of ice, tankers were unable to reach the terminal on Rügen for days and an icebreaker was needed. In addition, for technical reasons it is not trivial to send the gas quantities from the North and Baltic Seas across Germany to Bavaria, where gas is so urgently needed. Relying solely on the USA as an LNG supplier (more than 90 per cent of German imports now come from there) doesn’t really seem wise given the fragile political situation. Especially since gas plants in Texas froze because of the winter storm in January and prices immediately shot up because there were fears that delivery volumes would decline. ‘The LNG deliveries that the ministry constantly refers to come almost entirely from the USA. Europe is slipping into a dangerous dependency’, says Green Party politician Michael Kellner [well, you warmongers didn’t like the Russian gas].

In this case he also receives support from [chancellor Merz’] Union side. ‘We need greater diversification of suppliers’, says Andreas Lenz, economic and energy policy spokesman for the Union parliamentary group. A spokeswoman for the Ministry of Economic Affairs meanwhile points to storage facilities in Austria, which Germany could also tap into [I’m sure that will be a wonderful way forward—plus there’s the teeny-weeny problem that part of the gas in Austria is actually stored for other customers: how fast could Berlin screw up everything, you may infer? Well, if history is any guide…also, lest I forget, I wrote about Robert Habeck’s ‘new (gas) alliance’ between Berlin, Vienna, and Prague, if you can believe it, back in summer 2022]. How enthusiastic the neighbours would be in the event of an emergency is another question. Especially since EU regulations only provide for this in absolute emergencies [which I also detailed back in 2022: it’s now all coming together nicely, that is, for the warmongers and sociopaths in Brussels].

Who Should Pay For a Gas Reserve?

It is spring in particular that worries gas experts. From April onwards, the gas industry would have to start filling the storage tanks, which are actually empty this time, in order to meet the legal requirements. ‘Refilling will be challenging and possibly more expensive’, says the SPD’s energy policy spokesman, Armand Zorn [once again, Germany’s politicos™, in cahoots with the apparent ignoramuses in Brussels and their camp followers in legacy media, will point, once again, at evildoers elsewhere, such as Mr. Putin, of course Mr. Trump, and who knows what—before they’ll use a mirror: morons].

A paper on the gas supply situation is now circulating in the Union parliamentary group, which envisages examining a strategic gas reserve for Germany, ‘in particular to protect against disruptive events without creating market distortions’ [nothing says gov’t intervention being required for Mr. Market to function like this; it’s an admission that both hardcore post-Keynesian statists and the fake neoliberalistas will never accept: it’s obvious that what is needed isn’t more regulation but liability]. The Ministry of Economic Affairs is also currently evaluating a study on the ‘further development of filling level specifications in Germany and the EU’ and reports that it is in ‘deeper dialogue with the stakeholders in the gas industry’ [who, let’s not forget, is the Berlin gov’t in cahoots with the EU Commission: talk about navel-gazing galore]. Shortly before the committee meeting with Minister Reiche, the industry association BDEW also spoke out in favour of a national gas reserve as ‘a sensible instrument’.

What Might a Gas Reserve Look Like?

What this gas supply could look like in concrete terms is still completely open. Will there be, like in France, a further surcharge on the price of gas so that companies can fill the storage facilities? [let’s levy another fee on customers to pay for the solutions™ to gov’t-induced problems: aren’t we reminded of, say, the Climatology™ shit or, perhaps, the Roman Church selling indulgences to illiterate peasants was a bad and evil thing to do in Martin Luther’s days…]. Or should we hold the gas traders accountable and require them to maintain a reserve? Or should it be better done by the state? Any solution will be expensive [and these costs will be borne by John & Jane Q. Public, of course]. ‘More security of supply, more resilience, also comes with costs’, says CSU man Lenz [here’s a funny though: what about some consequences for the fucking morons who did this, ranging from acknowledgement of the US role in the bombing of Nord Stream, NATO expansion as the root cause of tensions with Russia, Ms. Merkel’s energy transition, and the Scholz-led bunch of idiots who decommissioned the nuclear power stations and the Green™ nonsequiturs in terms of energy policies? Without accountability, these mistakes™ will only compound].

This is a problem for the Federal Minister of Economics [if you’re not out of crocodile tears, please consider shedding one or two], after all, she has promised to reduce energy costs. At the beginning of the year, the gas levy for consumers has already been abolished, network fees are also set to fall, and a subsidised industrial electricity price is to be introduced [nothing says Mr. Market™ is a phony faker like these measures]. There is no need for market intervention, according to ministry circles [lol, please re-read the preceding sentence: this is late-stage Sovietism in action]. The market must ensure that the storage facilities are filled, and government intervention should only take place if this ‘sustainably increases security of supply, can be designed cost-efficiently and does not relieve market actors of their responsibility’ [so, what about accountability for the gov’t that’s so obviously incapable of designing shit?].

The reality on the gas market no longer has much to do with pure market economic theory. During the gas crisis, THE had to buy billions of dollars in gas in an emergency campaign to save Germany from the worst. At the same time, Uniper, Germany’s largest gas trader, was nationalised for billions, as was the storage operator Gazprom Germania, now Sefe [at the end of this piece, Die Zeit finally admits this: it’s gov’t turtles all the way down (apologies to turtles and tortoises)]. Gas expert Heinermann summarises the lesson from this time:

It is more cost-effective for the state to build up insurance with a state reserve than to have to take rescue measures worth billions in a crisis.

Bottom Lines

This is where this particular German Traumschiff (a pun deriving from the long-standing, cruise-ship themed telenovela, which Wikipedia notes was described by ‘a Variety magazine article [that] described the series as a “Love Boat”-like cruise liner skein.’[1]) is destined to go next: massive gov’t outlays, sadly to be done with more debt, perhaps EU-secured bills and bonds, higher taxes, fees, or what have you, and reduced gov’t services™ to stave off a future crisis like the one Germany (and Europe) is in.

Nothing in the above piece is actually new or couldn’t have been foreseen, which is why I’m merely posting a few of them below from, well, you can see the dates and understand that these pages here were a few years ahead of legacy media:

I’m posting these here to point out that all of this was clearly discernible before both the advent of the Russian ‘special military operation’ in Ukraine (Feb. 2022) and the Nord Stream bombing of September 2022.

Needless to say, yours truly has been chronicling this absurdity further, with particular reference being made to (drum roll):

Sadly, these things, while I’d argue that they are clearly visible to those who remain in reality-as-is, as opposed to reality™, have two major implications: it’s part and parcel of the US-China endgame in terms of all-out (hybrid) war against the one possible competitor (the EU), which emerged around 2000:

So, there you have it: this may not have been the desire/design by the EUrocritters and their camp followers in legacy media and across think tank-landia, but here we are.

I do propose one prediction here, which I believe to be fairly obvious:

If you thought the situation was very bad (and stupid to boot), I think we can be sure that the solutions™ that are being prepared—some becoming a bit clearer into view, as per the above Zeit piece—will only compound these problems.

Perhaps this will do the EU in, but I submit that to the EUrocritters, their answer (mantra) will never change: with ‘more EUrope’ being shouted from the top of their lungs, amplified by their camp followers in legacy media and across think tank-landia, the next, of course major™ and unprecedented™ push to transform™ the EU will emerge from the fog of war.

Speaking of war, this will be marketed as the only way to stave of a real war (which I fully expect to come out of this depravity), egged on by hawks in Washington, London, and Moscow.

Sic transit gloria mundi.

Great post!