The EU's Carbon Border Adjustment Mechanism 'Splained

'A tariff is a tax imposed by one country on the goods and services imported from another country.' ∽ Scott Nevil, via Investopedia

Today, we’ll do a follow-up on yesterday’s fertiliser-related content, if only because of this one little reference buried somewhere in the reporting™.

You see, the Austrian Chamber of Agriculture tried to assuage the public’s trepidations over the US-Israeli attack on Iran and its consequences by noting that there’s enough fertiliser available in Austria—and added this:

The early purchases of fertiliser are not related to the geopolitical situation, but rather to the EU’s Carbon Border Adjustment Mechanism, which caused uncertainty among farmers at the beginning of the year. The Carbon Border Adjustment Mechanism (CBAM) levies charges on CO2 emissions during the production of imported goods, such as fertilisers.

While I’ve added some emphases here, read the rest in case you’ve missed it:

For today, we’ll talk about the EU’s Carbon Border Adjustment Mechanism, or CBAM, which counts among the most recent innovations™ in this ever-weirder game of politicking™ in the EU.

If there are non-English passages in the following, the translation is mine; if not noted specifically, I’m using stuff that’s originally written in English, although all emphases and [snark] are mine.

Buckle up, this is a wild one.

A Brief History of CBAM (and Tariffs)

We’ll start out with a few snippets from its dedicated Wikipedia entry:

The EU Carbon Border Adjustment Mechanism (CBAM, pronounced /ˈsiːbæm/) is a carbon tariff on carbon intensive products, such as steel,[1] cement and some electricity,[2] imported to the European Union.[3] Legislated[4] as part of the European Green Deal, it took effect in 2026,[5] with reporting starting in 2023.[6][7][8] CBAM was passed by the European Parliament with 450 votes for, 115 against, and 55 abstentions[9][10] and the Council of the EU with 24 countries in favour.[11] It entered into force on 17 May 2023.[12]

As an aside (though it’s relevant): what’s a tariff?

As per Investopedia’s Scott Nevil, here’s a workable short-hand definition:

A tariff is a tax imposed by one country on the goods and services imported from another country to influence it, raise revenues, or protect competitive advantages.

It’s a tax as old as time, and everyone typically said so, from the Athenians of classical Greece to the present (Wikipedia has a rather longish section on esp. US tariff history).

The EU, however, being typically labelled sui generis—that is, in a meta category of its own and thus cannot be compared to other entities across time and space (‘The EU is often described as a sui generis political entity combining characteristics of both a federation and a confederation.[12][13]’, as per Wikipedia) has taken to calling a tariff (tax) a Carbon Border Adjustment Mechanism, or CBAM.

And we’ll soon learn as to how and why this was done.

And to do so, just a few more introductory lines are required (Wikipedia):

The price of CBAM certificates is linked to the price of EU allowances under the European Union Emissions Trading System introduced in 2005.[13][14] The CBAM is designed to stem carbon leakage to countries without a carbon price,[15] and also permits the EU to stop giving free allowances to some carbon-intensive sectors within its borders. All this should hasten decarbonisation.[16]

Once fully implemented, importers will be required to purchase CBAM certificates to cover the embedded emissions in their imported goods, creating a direct financial liability that varies week-to-week with ETS prices.[17]

Hence the need to briefly address the EU Emissions Trading System of 2005, which is basically a kind of financial shenanigans masquerading as both useful to combat climate change and raising additional revenues due to the sale of papers that derive their putative value from something else.

Careful readers noted the Italics in the preceding paragraph, which give away what the Emissions Trading System actually is: a bunch of derivatives as defined by, once again, Investopedia as follows:

A derivative is a kind of financial contract between two or more parties, the value of which fluctuates based on the price of one or more underlying assets. Traders can purchase these agreements and utilize them to hedge against risk, speculate on the asset’s movement, or leverage a position.

I’m not making this up, for technically = legally speaking, these emissions certificates are (drum roll), as per the EU’s very own words (section ‘market regulation’):

Legal Status of Allowances

Classified as financial instruments. The associated derivatives can hence be traded on secondary markets.

Their underlying assets are (drum roll) the EU’s emissions certificates, i.e., the right™ to emit CO2 whose price™ (fee) is determined by…well, the Emissions Trading System, or ETS, is a so-called ‘cap and trade’ scheme where the EU Commission determines the price per emissions allowance whose value is supposed to decrease over time, thus ‘putting a price on carbon’ (emissions) while, at the same time, regulating = increasing the price per emissions allowance.

In basic terms, it’s the perfect dialectic machine:

the EU decrees that CO2 emissions are a problem (thesis)

the EU sets up the ETS to fight climate change™ (antithesis)

once we get to 2039, the problem is solved™ by Mr. Market as (drum roll) no more such emissions allowances are issued, thus increasing their prices and incentivising polluters to do something (synthesis).

After 2039 no more allowances will be distributed. After the unused allowances will end also, no more emissions will be permitted.[2][136]

That above quote is the one-liner from the Wikipedia segment ‘Reaching net zero’, which gives away the game: if this would be a market-based solution, there would be enough of an incentive to for changes to emerge.

Since the entire thing is a political sideshow, however, it is obvious that if you have the political leadership decree stuff and its prices, what Mr. Market responds to are (drum roll) handouts and grift, as opposed to real world incentives.

And this isn’t a mere diatribe on the internet, here’s the give-away as formulated by the ETS’ Wikipedia entry’s sub-section on CBAM:

From 2026, the European Union is activating a carbon border tax [sic; I told you so] called Carbon Border Adjustment Mechanism (CBAM). The aim is to stop the problem of carbon leakage: the cost imposed by the European emission trading system making the European companies less competitive in comparison to foreign companies which do not make similar efforts for decarbonisation. As a result, instead of buying European products, the consumers in the European Union are buying imported products with high emissions, so instead of declining the emissions just travel to other countries and the European industry suffer losses. Therefore, with the help of this tax the European Union will force companies from other countries to pay similar price for carbon. This will permit to stop allocating allowances for free to hard-to-decarbonize sectors of the economy, which was done until now to prevent carbon leakage.[138]

While I’m kinda tempted to click on the ‘carbon leakage’ link, here’s the kicker: EU member-states pay high prices for goods and services due to higher costs, including for labour and regulations; some of these constraints to consumerism can be overcome by importing goods and services from outside the EU, which are cheaper due to lower energy, labour, and compliance costs—in short: ‘globalisation’.

To prevent this from happening, the hare-brained morons in Brussels dreamed up the above-related scheme to offset the price differentials (thereby eliminating the ‘comparative advantage’ of both outsourcing and import of said goods and services) by levying an import tax, or carbon tariff.

In consequence, EU subjects are milked twice: once because their formerly high-paying, unionised jobs in manufacturing went overseas into places with limited (ahem) such protections and way lower ages, hence these imported products have become cheaper, relatively speaking; upon importation, however, a new tariff is levied that is borne by the EU subjects who now have shittier jobs and lower wages.

Adding insult to injury, this is sold to the EU subjects as a measure to combat climate change or whatever while the same companies that now drastically lowered their cost per unit produced will simply roll over these tariffs (taxes) onto the consumer who is thus milked a third time.

And with these preliminaries clarified, let’s talk about the specifics, shall we?

CBAM in Action

And here we go (source):

The CBAM definitive period will start on 1 January 2026, therefore please read carefully and follow the instructions in the Authorisation Management Module section as soon as possible to submit your CBAM application. Importers of CBAM goods (or their indirect customs representatives) are urged to apply for the status of authorised CBAM declarants.

EU importers or their indirect customs representatives importing more than the single mass-based threshold of 50 tonnes of CBAM goods into the EU will have to apply for the status of authorized CBAM declarants. They will buy CBAM certificates from the national authorities in their country of establishment. The price of the certificates will be calculated based on auction price of EU ETS allowances expressed in €/tonne of CO2 emitted, as a quarterly average in 2026 and as a weekly average from 2027 onwards.

EU importers will declare the emissions embedded in their imports and surrender the corresponding number of certificates each year.

If importers can prove that a carbon price has already been paid during the production of the imported goods, the corresponding amount can be deducted.

I suppose that that third bullet point is where the fraud will occur: get a gov’t entity in whatever Third World country stuff is manufactured to issue such a declaration—and voilà, your EU-based reimbursement scheme is ready to go.

‘But, epimetheus, are you suggesting that our advanced, developed authorities are about as corrupt as the ones in these shithole countries?’

Of course I’m saying this, and if you cannot believe that to be true, well, that paragraph describes in a nutshell how certain elements defrauded the German finance ministry (of all places) of billions of euros:

It all happened before, and it will happen again, especially as the multi-layered nature of EU-issued carbon certificates that are supposedly checked by member-states’ customs officials add unnecessary complexity to the system akin to the federal/state-level kerfuffle in terms of oversight, compliance, and obfuscation (plus in the German case, the politico™ overseeing™ the fraud as Hamburg’s state finance minister was Olaf Scholz who, when the above story created its teapot-style tempest a few years ago had advanced to federal chancellor; you can clearly see how these shenanigans also define the EU/member-state shitshow).

But I digress.

What type of goods are concerned by CBAM?

The following goods are concerned by the CBAM regulation: cement, aluminium, fertilisers, iron and steel, hydrogen and electricity [note that this covers virtually all construction, agricultural production, and whatever else is manufactured in the EU/EEC].

Find more information specific to each of the 6 sectors under CBAM here.

For a list of goods that CBAM applies to, please check also the CBAM Regulation.

It’s not ‘just’ food we’re talking, for even if you’d be running, say, any kind of production facility abroad (powered by Green™ electricity), the EU will levy these tariffs (taxes) on whatever goods you produce.

This also puts a nail into the coffin of the (mostly fake) argumentation underlying the EU’s hare-brained Green New Deal: even if these CBAM tariffs (taxes) were a kind of industrial policy tool in disguise (which I doubt they are), it’s hard, if not outright impossible, for whatever goods and services to be created in the EU out of nothing but hot air.

The main problems will arise due to this clause:

Non-compliance: Importers and indirect customs representatives may face delays and penalties that could disrupt their supply chain.

In case anyone misbehaves, the EU Commission will punish both importers and member-states’ customs agencies by levying fees etc.

The by far most absurd file in this scheme is the ‘Guidance document on CBAM implementation for installation operators outside the EU’, which is available in multiple languages and a mere 252 pages long. I’ll delimit myself to some of the most patently absurd regulations the EU is trying to force on the rest of the planet:

Are you exporting your goods to customers in EU Member States?

The CBAM affects you if this is the case.

Please note that your products may also be purchased by clients who themselves manufacture CBAM goods, and your products may serve as “precursor” for their CBAM goods, which then may be exported to EU countries. Also, if you sell your products to traders who then sell them to EU customers, your goods fall under the CBAM [there’s no way out of the CBAM scheme, even if you don’t even know (or care) who your ‘precursor’ products are sold to because (drum roll)]

In all those cases where CBAM goods end up in being imported into the EU, at some point the importer will contact you to gather information on the “embedded emissions” of these CBAM goods. Alternatively, the operator using your goods as precursor for producing other CBAM goods will ask the level of embedded emissions. Therefore, you must be prepared to provide these data and as soon as possible start to develop a monitoring methodology at your installation, as described in this guidance document [all on p. 12].

The admittedly ingenious sleight-of-hand is that these CBAM tariffs (taxes) will be levied at the port-of-entry into the EU/EEC, but the EU Commission is making any supplier for anything that might eventually end up in the EU/EEC to abide by these regulations.

Let that sink in.

Imagine, if you will, a EU-headquartered company with subsidiaries in, say, Vietnam whose sub-contracted manufacturers produce, say, nuts and bolts (or whatever). Because of CBAM, that sub-contracted manufacturer (which uses Vietnamese electricity to run its plant) will have to comply with the CBAM reporting and compliance regulations, if only to document that the electricity its sub-contractor uses is either of the Green™ kind and/or document everything so that some EU agency can determine the surcharge upon importation into the EU/EEC of these nuts and bolts.

You can run the same thought-experiment with, say, a US car company that outsourced its manufacturing to sub-contractors in Canada and Mexico.

And that’s what deduced before you read the paragraphs on ‘embedded emissions’ (which are on pp. 12-13, footnotes omitted):

What are embedded emissions? The concept has been developed to reflect as much as possible the way in which emissions are covered by the EU ETS if the CBAM goods were produced in the EU. The EU ETS requires operators to pay a price for their own (“direct”) emissions. However, if they consume electricity, they also experience the CO2 costs included in the price of electricity they purchase (“indirect emissions”). The same applies to the input materials needed for their production process, and which may be supplied by an EU ETS installation. These so-called precursors therefore contribute to the CO2 costs the EU ETS installation faces. The “embedded emissions” are defined in parallel to the emissions causing CO2 costs in the EU ETS: they take into account the direct and indirect emissions of the production process as well as the embedded emissions of precursors. They are similar in concept to a carbon footprint of the goods. The scope of the CBAM is principally related to the rules of the EU ETS and therefore has differences to other methods for calculating product carbon footprints such as the “GHG Protocol” or ISO14067.

There follows a multi-level, segmented listing of all the stuff that manufacturers and suppliers are required to monitor and disclose (pp. 13-16); there is another such listing of mandatory reporting requirements for manufacturers (pp. 23-25), followed by a similar listing for importers (pp. 25-27).

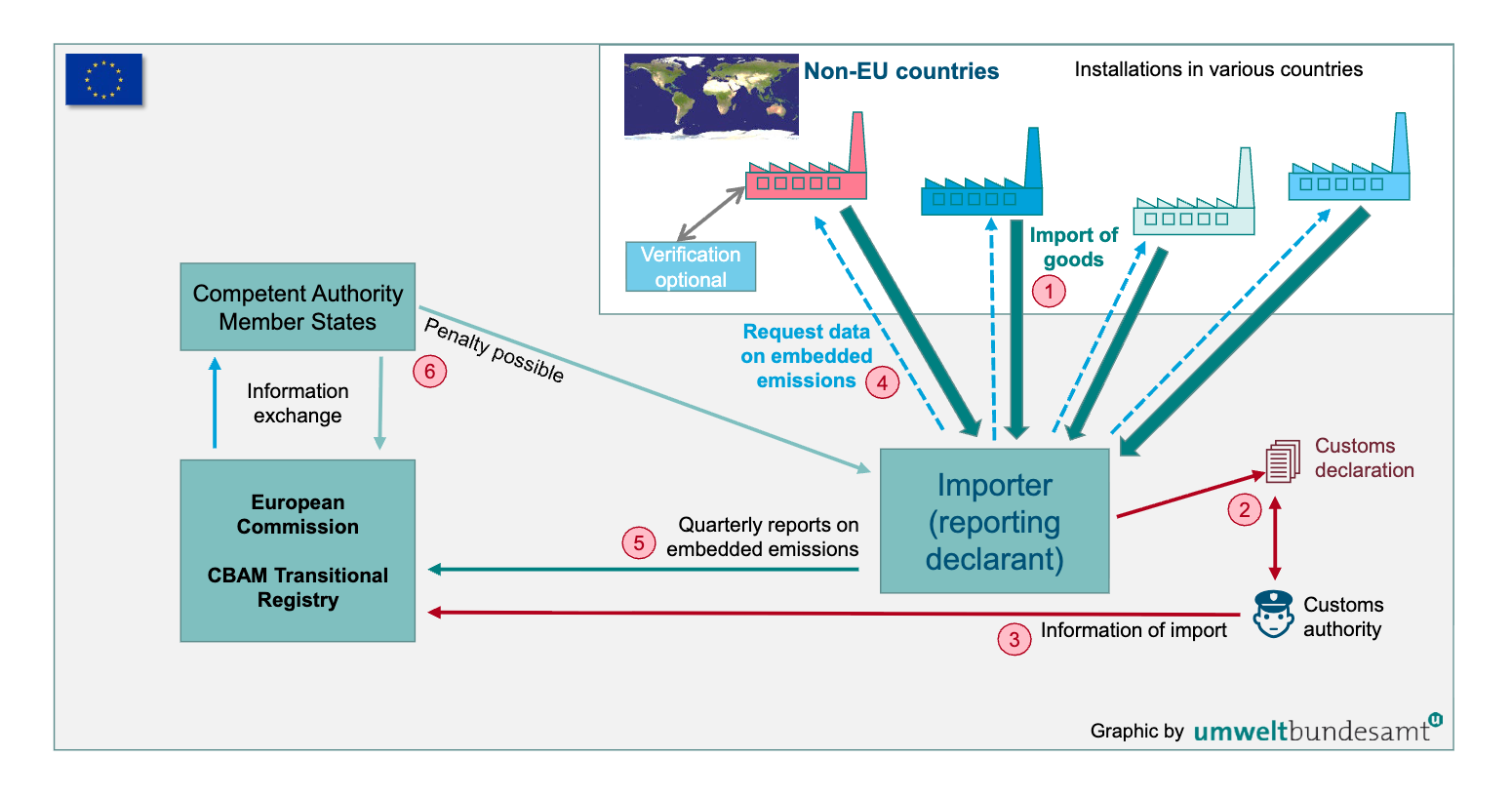

If this is mind-boggling, p. 28 holds this wonderful illustration that ‘splains it all (albeit schematically for the transitional period that ended on 31 Dec. 2025 and there’s no corresponding figure yet available):

I’ll wrap this up with the summary (p. 7) ‘splaining what this legally non-binding 252 pages-strong guidance™ is telling you:

The Carbon Border Adjustment Mechanism (CBAM) is an environmental policy instrument designed to apply the same carbon costs to imported products as would be incurred by installations operating in the European Union (EU). In doing so, the CBAM reduces the risk of the EU’s climate objectives being undermined by production relocating to countries with less ambitious decarbonisation policies (so-called ‘carbon leakage’).

Under the CBAM, in its definitive (post-transitional) period EU authorised declarants representing the importers of certain goods will purchase and surrender CBAM certificates for the embedded emissions of their imported goods. As the price for those certificates will derive from the EU Emission Trading System (EU ETS) allowance price, and since Monitoring, Reporting and Verification (MRV) rules have been designed based on the MRV system of the EU ETS, this will equalise the price of carbon incurred between imported goods and goods produced in installations participating in the EU ETS.

If your head hurts now, welcome to the club.

Bottom Lines

CBAM is a tariff (tax) scheme involving the EU Commission determining prices and regulatory burdens whose implementation is farmed out to both the EU/EEC member-states customs agencies and all companies at all levels further down the supply chain.

It all boils down to this:

If you wish to sell your stuff to the EUroturds, or EUretards, you’ll all be subject to the same regulatory/tariff régime as the subjects of the EU.

You don’t have to join the EU/EEC to be subject to the whims of the Brussels-based nomenklatura.

At a macro level, though, this is the next step—rather: a gigantic leap—towards the actualisation of two major aspects:

establish a global regulatory framework for everything

permit the nomenklatura that establishes said framework to effectively regulate prices, which affects demand, which permits the nomenklatura to direct both production (via tariffs) and consumptions (as these fees are rolled over onto customers everywhere)

In other words: the EU was a kind of neoliberal/globalist pet project to begin with, and now that the neoliberal/globalist revolution has run its course far enough, it will start devouring its children (consumers).

In short: neoliberalism/globalism is entering its Jacobin phase.

I doubt that European citizens will muster enough spine to fight this kind of taxation without representation.