The EU's '28th Regime'

Pushing the boundaries of what is legal and possible, Brussels is pushing full-steam ahead on the next major integration™ push

Yesterday, we talked about Germany, perhaps the sickest of inmate of Europe’s asylum for the politically insane. The rot that’s been spreading for some time now, though, has been festering—and now, that particular cancerous growth on the European body politics has metastasised beyond belief.

Exhibit A here is the recent—did you notice it anywhere?—‘informal’ meeting of the EU Council (a summit meeting of all EU heads of gov’ts) in Alden Biesen, Belgium:

Here is a laundry list of its achievements/visions:

The leaders were joined by Mario Draghi for a working session on EU competitiveness in a new global geoeconomic context, and by Enrico Letta for a working session on how to make better use of the single market in a fast-changing world.

Looking ahead, the leaders agreed on a set of priority areas to strengthen EU competitiveness and strategic autonomy. They will follow-up on these discussions at the upcoming European Council meeting in March, at which point the Commission is also expected to present a roadmap on ‘one Europe, one market‘.

The President of the European Council, António Costa, summed up the leaders’ discussions in a speech following the meeting…

Simpler EU rules for businesses

A deeper EU single market

Investments and Innovation

Energy

Strategic Industries

Open trade policy

There are some links to background information on these points, but no minutes or the like have been published. Apparently, this isn’t a ‘need to know’ for the hoi polloi.

‘Moving Forward on a “28the Regime”’

Under the bullet point of ‘a deeper EU single market’, however, the following reference was explicitly made:

In this context, the leaders also agreed on the importance of moving forward on a '28th regime', to ensure that EU companies can operate seamlessly across borders within a single set of corporate rules. This in turn can help companies grow across Europe, reduce administrative burdens and ease access to financing.

The emphasis being theirs in the original, have you ever heard about this?

It’s proximal origin appears to be Von der Leyen’s state of the EU speech delivered on 10 Sept. 2025, in which she said, among other things (emphases in the original):

Our proposals will cut EUR 8 billion a year of bureaucratic costs for European companies. A digital Euro for example will make it easier for companies and consumers alike. And further omnibuses are on their way – for example on military mobility or digital. For innovative companies, we are preparing the so-called 28th regime and speeding up the work on the Savings and Investments Union. Because we have many high potential startups in key technologies like quantum, AI or biotech. As they grow, the limited availability of risk capital forces them to turn to foreign investors. This is wealth and jobs going elsewhere. And it jeopardises our tech sovereignty.

Note the condescension, focus on what she says: ‘further omnibuses are on their way’, meaning that stuff that’s unrelated to one or the other EU Law™ will be attached to it (mainly, I’d argue, because that stuff wouldn’t pass muster otherwise).

There’s, of course, the unavoidable central bank digital currency™ (‘a digital Euro’), which cannot work without mandatory digital ID.

Yet the most egregious sentence may be this one:

For innovative companies, we are preparing the so-called 28th regime and speeding up the work on the Savings and Investments Union.

While here you may find background on the Savings and Investments Union, its true colours are there for everyone to see:

Yep, the EU Commission wants to your ‘household savings’ to ‘be invested in the capital markets’—aren’t there any pension funds left to loot?—and the ruse they are using is that SMEs ‘often struggle to secure financing from banks’.

Perhaps the EU should implement strong anti-trust proceedings and reverse the ongoing cartel-building of the ECB’s ‘primary dealers’, the ‘too-big-to-fail’ banks? But, no, Von der Leyen wants your ‘household savings’ funnelled towards the ‘growing investment needs of the EU economy’. Go figure.

Background in the linked piece below:

As regards the ‘28th regime’, finally, here’s what that means for those who haven’t been paying attention, and, of course, we’ll let the EU politicos™ and their camp followers ‘splain this to you in their own lingo.

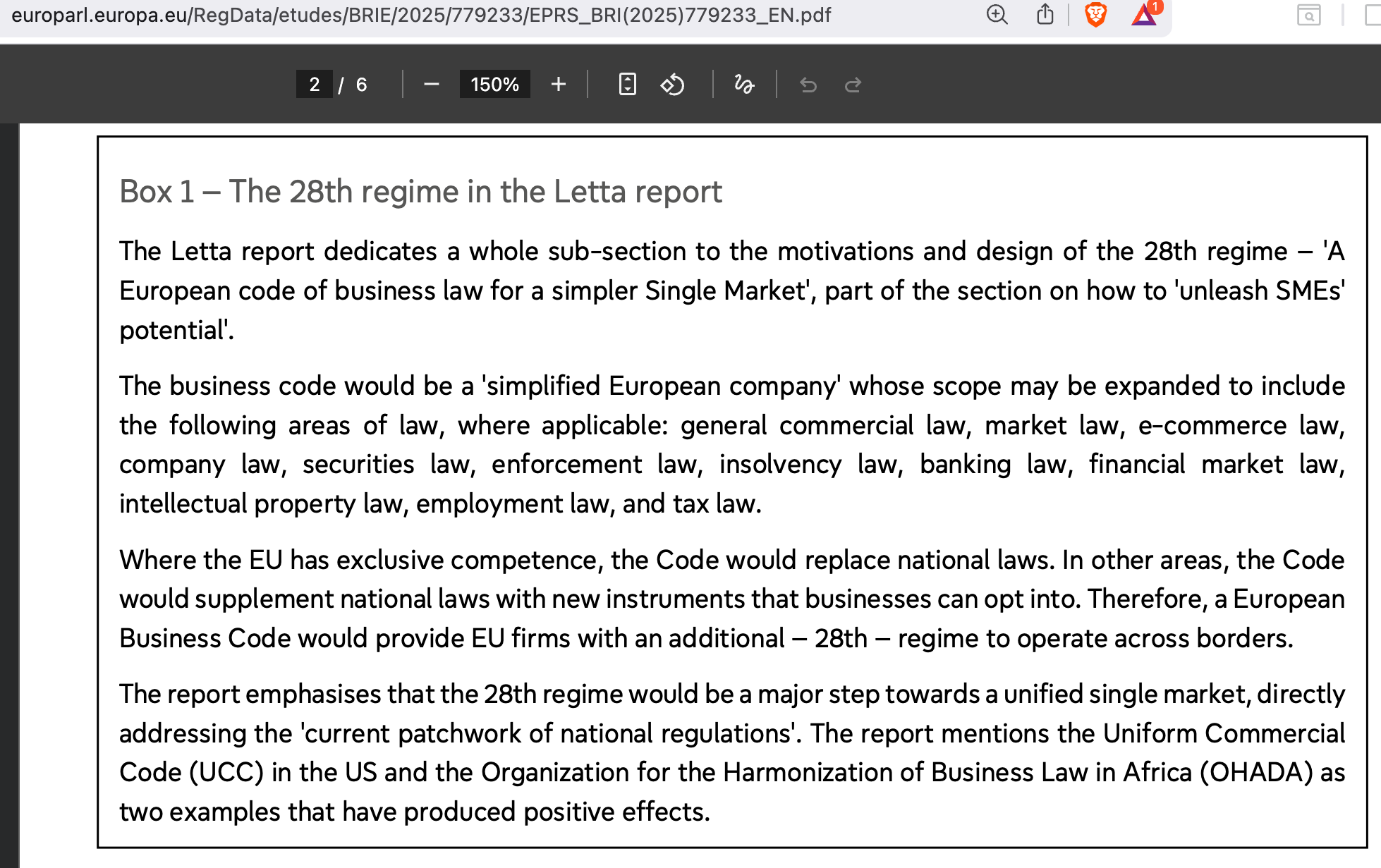

Hence, dear readers, please welcome Clément Évroux and Issam Hallak of the European Parliamentary Research Service who, back in the stone age days of December 2025, co-authored a report entitled ‘The 28th Regime’, which you can find on the EU Parliament’s website (here and in the following, emphases and [snark] mine):

Summary

Although it is a long-standing concept, the 28th regime was emphasised by Enrico Letta’s report in 2024 as a major recommendation to reinforce the single market and remove internal barriers. The International Monetary Fund estimates that the persistent barriers to the EU single market still represented the equivalent of a 110 % tariff on services [maybe so, but the point is: cui bono, who benefits?].

The 28th regime, which has yet to be defined, would possibly be a specific legal framework that would govern various aspects of businesses that opt into the scheme from ‘birth to death’, such as establishment, organisation, operations, and disputes.

The Commission made the 28th regime a key element of its competitiveness compass, under the ‘necessity’ of closing the innovation gap [from ‘missile gap’ of the 1950s and 1960s (which was fake) to other such ‘gaps’, that’s always been a ruse]; the legislative proposal is scheduled for the first quarter of 2026. The start-up and scale-up strategy published in June 2025 will encompass the 28th regime, which will be aimed at young and small innovative companies. The scope would thus be narrowed substantially compared with Letta’s recommendations.

The European Parliament is currently engaged in preparatory work on the 28th regime.

So, it’s basically another set of rules for businesses (legal persons) while the likes of you and me are stuck in the real world, warts, taxes, reams of bureaucratic regulations, and all.

While I highly recommend the report—and we’ll discuss its contents further in the coming weeks—the key section, I’d submit, is perhaps the one espousing ‘the stakeholders’ views’ (read that aloud mimicking Klaus Schwab):

The 28th regime initiative is widely welcomed by industry representative organisations as a way of simplifying rules for firms, with some reservations, mostly in relation to large versus small companies. Other organisations are particularly concerned about the ‘forum shopping’ such a new regime may create, which could affect domestic laws, such as those on labour and taxation.

Who could have guessed that, eh?

Here’s a bit more™ on this nonsense, straight from the horse’s mouth:

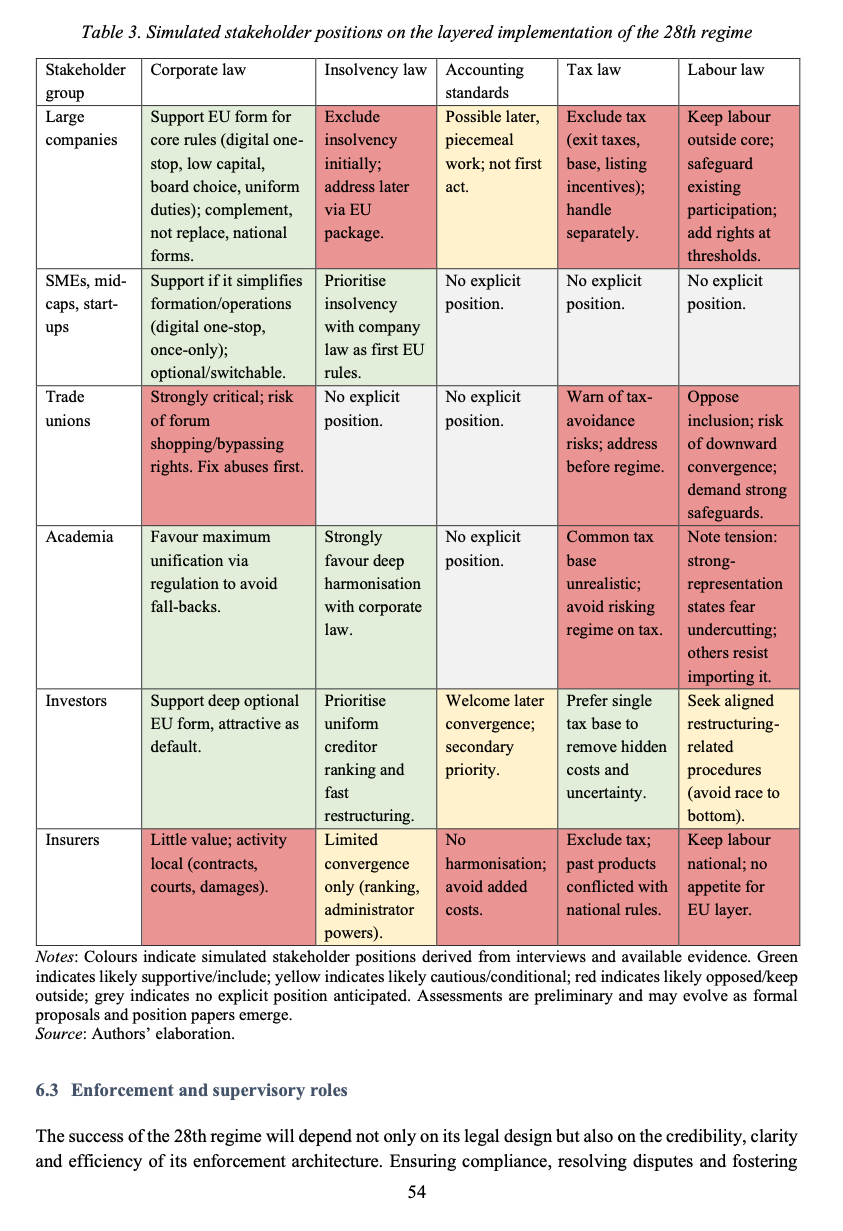

Speaking of ze stakeholders, a study by Ecorys and the Centre for European Policy Study (CEPS)—commissioned, no less, by the European Economic and Social Committee and published in October 2025—offers some insights into the thinking of the EUrocrats, or, in the lingo of the Clément Évroux and Issam Hallak, ‘provides a comprehensive analysis of the concept, rationale, historical evolution, and prospects of the 28th regime in EU law’.

Fun facts of that paper include, among others, that the term ‘citizen’ appears a mere three times while the term ‘stakeholder’ is mentioned 52 times.

And then there’s this gem, tucked away in Table 3 on p. 54: note the caption, which gives away the ‘game’, or ‘simulation’, that these findings™ are based on:

Spotted any ‘citizens’? Me neither.

There’s so much nonsense in this study™, it boggles the mind, yet it’s highly, highly dangerous and is poised to erode away the remnants of sovereignty under the conditions of this new stakeholder-centric 28th regime:

6.4.1 Legal coexistence through a two-tier framework

A foundational feature of the 28th regime approach is its coexistence with national frameworks. This two-tier model offers firms the flexibility to choose between a harmonised EU-level framework and domestic legal systems, preserving subsidiarity and reducing political resistance. However, for this arrangement to function effectively, the interface between national and EU frameworks must be clearly delineated. In particular, firms that opt into the 28th regime must not be subject to overlapping or duplicative national rules in the same regulatory domain.

Your taxes will still be funnelled towards that ‘28th regime’, even if you, puny citizen, may not ‘opt-in’ that legal framework.

As an aside, the term ‘citizen’ never appears once in the EU Parliament’s report.

Fun fact, the concluding paragraph reads as follows:

Long-term success of a 28th regime depends not only on its legal merits, but also on the credibility of its implementation roadmap. A phased, flexible and transparent rollout—supported by iterative learning and institutional accountability—can turn an ambitious legislative proposal into a politically sustainable and operationally workable reality.

Funny that, too, one the EU’s greatest achievements (the Single Market) and its gargantuan EU Commission bureaucracy, ostensibly necessary™ to ‘harmonise’ standards, rules, and regulations across 27 member-states, has failed. There’s no other way to view this shitshow, for if that EU régime would be working fine and dandy, there’s no need for a ‘28th regime’.

Incidentally, that’s not merely my opinion but also the stance of the European Trade Union Institute, citing threats to labour rights while such a new ‘business code’ would create several issues, including ‘forum shopping’—a race to the bottom in terms of which jurisdiction offers more loopholes—and calling it, in effect, ‘unnecessary’.

Bottom Lines

None of the above comes as a surprise to your humble correspondent, dear readers, partially because these seemingly obscure studies, papers, and reports are, sadly, highly relevant yet hardly-ever discussed in legacy media.

Yet those who read them have a significant advantage as they tell you what they wish to do well in advance; take, for instance, the late Wolfgang Schäuble, Germany’s former Minister of Finance and later president of the Bundestag, who back in 2011, spoke the following words in public:

European unification is to create a new form of governance, where there is not one level that is responsible for everything and which then, in case of doubt, confers onto others certain policy areas through international treaties. I am firmly convinced that this is a much more forward-looking approach for the 21st century than a relapse into the regulatory monopoly of the classical national state of past centuries...

I would like to make it quite clear to you that I am quite convinced that in a period of less than 24 months we will be able to change the European regulatory framework in this way. We just need to amend Protocol 14—whoever wants to read it, in general, in the Lisbon Treaty—in such a way that we create on it the broad outlines of a fiscal union for the eurozone.

I’ve discussed the implications of informal meetings and esp. the preparatory work carried out by appointees and otherwise contracted experts™ elsewhere, hence I’ll delimit myself to citing Art. 1 of said Protocol 14 of the Lisbon Treaty:

The Ministers of the Member States whose currency is the euro shall meet informally. Such meetings shall take place, when necessary, to discuss questions related to the specific responsibilities they share with regard to the single currency. The Commission shall take part in the meetings. The European Central Bank shall be invited to take part in such meetings, which shall be prepared by the representatives of the Ministers with responsibility for finance of the Member States whose currency is the euro and of the Commission.

By the time you’re reading this paragraph, we note, therefore, that the hierarchy established by the Lisbon Treaty’s Protocol Nr. 14 appears to be as follows:

EU Commission, ECB + reps of the Finance Ministers ≠ Economy and Finance Ministers Meetings (that working group’s acronym would be ECOFIN) > member state governments > national parliaments

Do you see it yet? This is the ‘normal’ way EU Law™ is created since 2007, and these experiences underlie the ways and means the EU Commission is going to bring about their ‘28th regime’.

‘More’ may be read-up on in the below-linked piece

I’ll let Ursula Von der Leyen have the last word here (for now), with another nugget of wisdom as regards the ambition of the EU Commission (again from her ‘state of the union’ speech of 25 Sept. 2025):

Our greatest asset is the Single Market—but it remains unfinished. The IMF estimates that the internal barriers within the Single Market are equivalent to a 45% tariff on goods. And a 110% tariff on services. Just think of what we are missing out on. And, as underscored by the Letta report, the Single Market remains incomplete, mostly in three domains: finance, energy, and telecommunications. We need clear political deadlines. This is why we will present a Single Market Roadmap to 2028. On capital, services, energy, telecoms, the 28th regime and the fifth freedom for knowledge and innovation. Only what gets measured, gets done.

It’s all ‘there’ for you and me and everybody to see.

Don’t say they’ve not been telling you what they plan to do.

Incidentally, I think that this ‘28th regime’, while a big boondoggle for big business (to tap into ‘unused household savings’), has actually a quite different meaning for the EU Commission and their partners-in-crime over at the ECB:

the EU Commission has no money to spend, let alone any income. The issuance of ‘EU-Bonds and EU-Bills’, then, turns the EU Commission into a de facto ‘sovereign issuer’, which means that this is the backdoor through which ‘Brussels’ can raise funds from their ‘primary dealers’ and spend without either a written constitution or the authority to tax the EU population directly…

If, at this point, you’re asking who or what is underwriting these ‘EU-Bonds and EU-Bills’, there are but two options: either the EU Commission securitises its five-year budget…and/or otherwise put ‘something else’ aside to secure these ‘EU-Bonds and EU-Bills’.

Please read the rest here:

Back in late August 2025, I was unsure if that ‘something else’ would be a are EU Treaty or something cooked up using the Lisbon Treaty’s Protocol 14.

Now, I believe the fog of war has cleared a bit: it looks like that ‘28th regime’ will require a kind of ‘pay-to-play’ subscriber fee—i.e., call it taxes™ or whatever—that permits the EU Commission as overseer-in-chief to securitise its EU Bills & Bonds with regular income streams.

The way forward is, it would seem, to bypass whatever legal™ constraints there may be (in the EU Treaties) and move virtually everything controversial™ into that ‘28th regime’ to bypass all oversight.

Nothing about the most likely outcome (which I wrote back in August 2025), however, will change:

Since the Commission is not responsible to any kind of judicial, parliamentary, or other oversight, this is a recipe for abuse, corruption, and political adventurism (disaster).

The writing is getting ever more clearer on the wall.

Two points ; EU Bills and Bonds : they are not talking about bonds, since bonds are linked to specific assets and the EU has none. They are talking about debentures. Debentures are a bet on the general credit of the issuer. It is a major difference. It means that in case of a sovereign issuer, it has the possibility to raise taxes to pay the creditors and the sky is usually the limit. Now, the second point, and it is a funny thing ; the fiscal union. We have to go back to Milton Freidman and the Euro who, years ago warned the EU that a monetary union without a fiscal union was an impossibility. Why ? It is because the budget of each State is independent, the spending are decided by the national parliament of each country. You are always at risk of not printing enough money and it is exactly what is happening in Europe. The center, in this case Bruxelles, doesn’t controlled anything and this, is leading to dramatic budget imbalance and endless printing of money by the ECB which is a failed bank, depending itself of the Bundesbank. Do you see where all of this is going ? It is ultimately an attempt to control national budget, national parliament rubbing stamping what Bruxelles will allow them to get as part of the supra-national European budget. At the same time, Bruxelles will have the ability to raise as much money as desired through the issuance of debentures, for the various pipe dream projects the bureaucrats in Bruxelles, have on their mind and to tax as much as required to pay the creditors.

If the EU wanted to be succesful, you know what it ought to do?

Scrap the entire thing and re-form by simply importing the US Constitution and Bill of Rights as is, but applied to Europe, incorporating only the first ten amendments to the Constitution.