EU in Recession Since 2022

A new report by the think (sic) tank Credireform traces corporate and SME insolvencies--they are on the rise since 2022

Time to see how (far) off my writings of yesteryear were—let’s start with the below piece from summer 2022:

Back then, I proposed that four macro trends would run amok in parallel:

More centralisation, which also means enormously increasing administrative overhead costs

Bigger, and fewer, mega corporations running everything…small and medium-sized enterprises will…be gobbled up by the global behemoths

Supply shocks are coming, and we’ll see them in terms of high prices for everything (did anyone mention ‘tariffs’ yet?)

Services, widely understood, will contract spatially. By this, I mean that while the past decades (esp. since 1945) were marked by the ever-quickening expansion of human affairs into even the remotest corners of any country, we’re about to embark on the reversal of these processes

In my ‘bottom lines’, I made the following comment:

The ‘West’ in its present configuration is perhaps unique in both its leaders’ rejection of reality and the (so far) absence of any consequences.

Please read up on the somewhat long-ish piece, if you’re longing for ‘more’ particulars by clicking on the link below:

And with the stage thus set, let’s do a reality check and learn about the world as it is in spring 2025.

The below is from the quarterly report (Q1, 2025) of the Vienna-based marketing, PR, and consultancy agency Creditreform (which translates into ‘Lending Reform’), which issued its first such report a few days ago (in German only).

Translation, emphases, and bottom lines mine.

Insolvencies in Western Europe in 2024

By Creditreform, Q1 2025, 6 May 2025 [source]

In 2024, the European economy recorded only modest economic growth in a generally difficult global environment. The pace of growth slowed noticeably over the course of the year—in some countries, such as Germany, the economy stagnated or even contracted [hi there, recession, at the very least]. The main reasons for this development were high energy prices [high time to ban the import of Russian gas, as Von der Leyen is about to] and geopolitical uncertainties [better antagonise some more countries: here’s looking at you, China]. The main industrialised countries in particular suffered from a weak economy—in some cases even from an ongoing industrial crisis [oh, well, stupid domestic policies made things worse, esp. the Covid mandates]. The monetary policy of the European Central Bank (ECB) remained focused on curbing inflation, but had a negative impact on investment activity—particularly in the construction and property sectors [here, we might need to mention that most countries are built up well beyond the needs of the coming population decline, to say nothing about asset inflation in the real estate sector]. At the same time, economic uncertainty and falling real incomes weighed on consumer sentiment and led to restrained demand…

Trends in Western Europe in 2024

In Western Europe—defined here as the EU-14 states [i.e., before the accession of Eastern Europe after 2004] plus Norway, Switzerland and the UK—there was another increase in corporate insolvencies in 2024. The number of bankruptcy filings rose by 12.2% compared to the previous year to a total of 190,449. Although the percentage increase was lower than in 2023 (plus 20.9 per cent), the number of insolvencies is higher than it has been for over a decade. Over 190,000 bankruptcy filings represent the highest level since 2013, when around 192,800 corporate insolvencies were recorded as a result of the financial crisis of 2008/2009 [give it time, we’re getting ‘there’ before too long, perhaps with or without a ‘formal’ stock market crash].

Since the previous low point in 2021 with only 112,686 insolvencies, corporate insolvencies in Western Europe have increased by almost 70 per cent—and a further increase seems foreseeable [bye-bye recession, hello depression]…

Various crises—including increased energy costs, high inflation, and the after-effects of the coronavirus pandemic [as if the latter’s ‘after-effects’ fell from the sky on a Monday morning: once more, we note the absence of the human-made qualities of said ‘after-effects’, i.e., shitty policies]—have weighed on the economic stability of many companies. At the same time, urgently needed increases in earnings failed to materialise [i.e., if only people would have ramped up consumer spending].

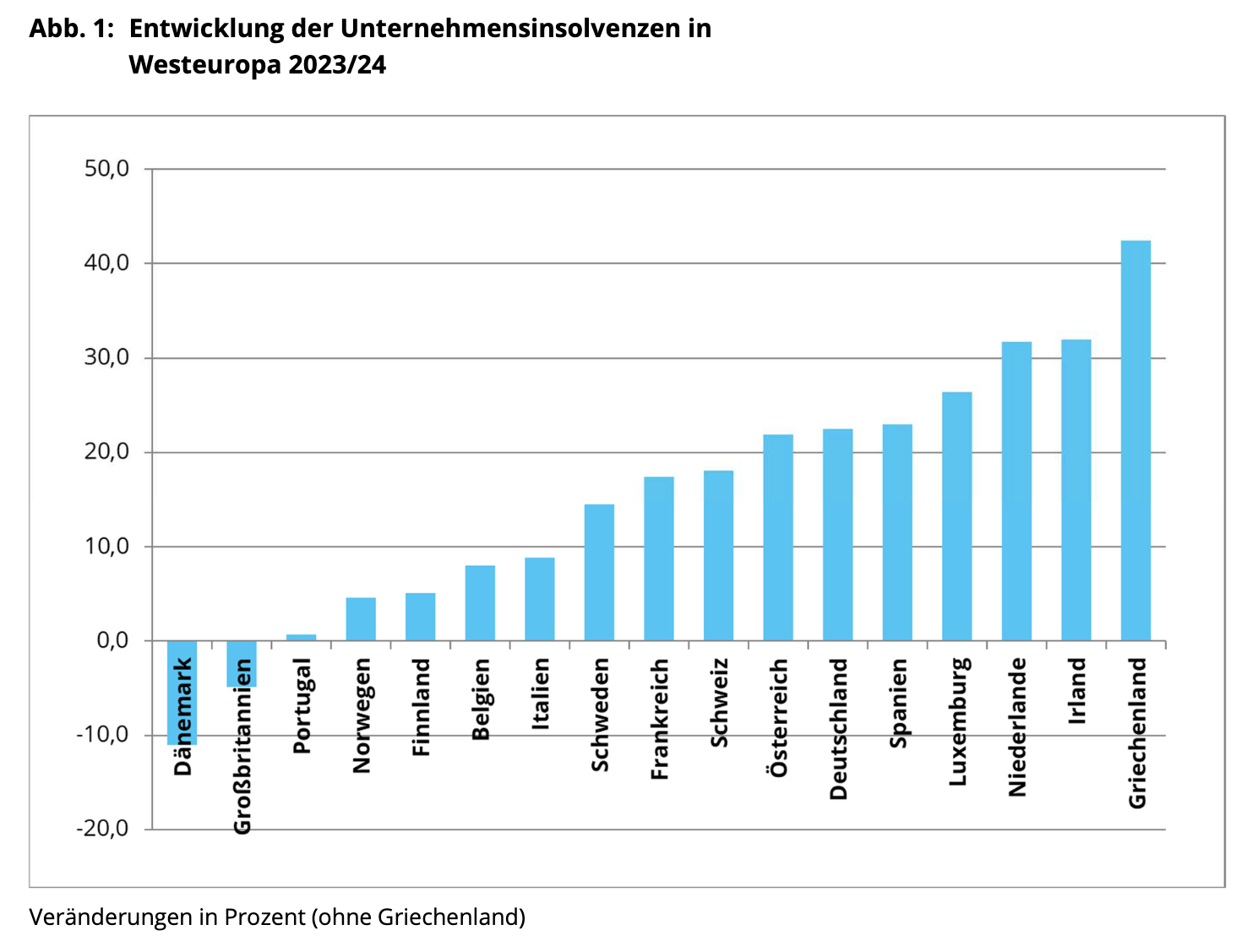

Fig. 1: YoY Changes [in %] of Bankruptcy Filings in Western Europe

With the exception of Denmark and the UK [wasn’t ‘Brexit’ going to destroy the UK economy?], all Western European countries analysed recorded an increase in corporate insolvencies in 2024 (see Fig. 1). The increase was strongest in Greece (plus 42.5%). It was followed by Ireland (up 32%), the Netherlands (up 31.7%), Luxembourg (up 26.4%) and Spain (up 23%).

The number of filings also rose significantly in Germany, Austria, Switzerland, and France—in the double-digit percentage range in each case. In contrast, the rise in insolvencies was less pronounced than the Western European average in countries such as Portugal, Norway, and Finland…

In almost all of the countries analysed, the number of cases is now well above the 2019 reference value, which was used as a pre-coronavirus comparison in this analysis. In Scandinavia, Germany and the Benelux countries, too, insolvency figures now exceed the 2019 level. In Italy, on the other hand, they remain below [huhum, isn’t this prima facie evidence of something?]…

Compared to 2019, France and the UK have become more important for insolvency activity in Western Europe. The relative contribution of the Scandinavian countries, on the other hand, is declining.

Fig. 3: Relative Distribution of Insolvencies (in %); dark blue = Scandinavia; red = Germany; turquoise = France; light green = UK; purple = Italy; grey = Spain; light blue = all others (excl. Austria, which is blue)

A Reality-Check (on my 2022 piece)

The above chart helps us to put the relative increases in the various countries into perspective: it’s way worse in the bigger economies of France and Germany than, say, in Spain or Italy.

Isn’t it amazing that the ludicrous wannabe Napoleon currently pretending to be running France is presiding over a massive rise of insolvencies while threatening™ Russia? I mean, the mis-match between facts (economic decline) and fiction (Mr. Macron’s lunacy) is palpable. Comparable notions are true for both the UK and Germany, too, hence questions must be asked about the stewardship of these countries in the past decade.

Across various industries, the numbers are equally bad, albeit unevenly distributed (all percentages relate year-on-year changes to 2023):

manufacturing insolvencies rose by 9.3% in 2024

construction insolvencies rose by 15.4%

retail insolvencies rose by 8.1%

and insolvencies involving services rose by 14.2%

And this is how Creditreform spins this:

Following the massive decline in insolvency figures during the 2020/2021 coronavirus pandemic—due to one-off effects [i.e., massive gov’t hand-outs for businesses to stay afloat]—a trend reversal set in from 2022. Since then, the number of cases has risen again significantly in all economic sectors [oh my, my summer 2022 piece was—112% correct]. This trend also continued in 2024. Insolvency figures are now above the pre-corona level of 2019 in all sectors [we used to call such a situation an economic crisis]. This increase is particularly evident in the construction and service sectors. The trend has now also spread to the manufacturing industry, where the number of insolvencies in 2024 was just above the 2019 reference value.

In case you’re wondering how bad the situation is, well, here’s a few choice quotes from Austrian state broadcaster ORF whose journos™ spin the above.-related Creditreform report as follows (article dated 6 May 2025):

According to Creditreform, this is the longest phase of economic weakness in around 30 years…

Creditreform expert: ‘Further increase on the horizon’

‘Three years of stagnation and economic doldrums are not only affecting Germany,’ says Patrik-Ludwig Hantzsch, Head of Creditreform Economic Research in Germany. Europe as a whole is suffering from weak economic development...

In Central and Eastern Europe, too, there were more corporate insolvencies in many countries in 2024, although the number of cases was often still below the pre-CoV level of 2019. 39,681 cases were registered in Central and Eastern Europe in total, compared to 64,917 in the previous year. Poland, Latvia, Slovenia, Lithuania and Estonia recorded particularly significant increases. Meanwhile, Hungary recorded significantly fewer corporate insolvencies and thus had a significant impact on the overall picture.

Isn’t it interesting to note that both Italy and Hungary—both governed ostensibly by far right-wing loons™—performed far better than their more socialistic peers? It’s very telling that this aspect remains literally unmentioned.

How does the US compare? Well, there’s also a concluding paragraph that offers some information:

The number of insolvencies in the USA increased by 16.6%. ‘Despite moderate economic growth, high interest rates and declining consumer spending continue to weigh heavy on companies’, explained Creditreform. However, the US insolvency filings remained below the level of the pre-CoV years 2018 and 2019.

Bottom Lines

Europe is deep in the shithole, with its leaders™ continuing to dig and enjoying it.

There’s little else to note but the fact that the EU was sold to the various peoples of Europe as bringing peace and prosperity.

With the current war-craze vs. Russia and China, the notion of peace is rapidly receding from everyone’s eyes.

Given the hell-bent drive towards the bottom in terms of energy policies, Europeans are currently bidding farewell to the prospect of prosperity.

What do you think will happen once bread lines form again?

I suppose the evil™ act of burning EU flags and angry mass protests will come as a shock to most normies, esp. those morons in Brussels.

This is what I wrote in summer 2022:

The ‘West’ in its present configuration is perhaps unique in both its leaders’ rejection of reality and the (so far) absence of any consequences.

Once this changes, we will also put better people in charge, perhaps by means of elections, but I could also imagine that future leaders will ‘emerge’ by virtue of their skills, character, or accomplishments again. Once consequences will return to politics and life in general, the morons who are currently pretending to be in charge will quietly recede from view as they have neither the intellectual capacities to govern nor the endurance required (to say nothing about a sense of shame).

I’ll throw in one more aspect: that transition to reality will neither be very calm nor without dislocations. If the latter will come in the form of a Russian rocket, I wouldn’t be surprised as Germany’s new loon-in-chief Friedrich Merz has said repeatedly that he’d hand over Taurus cruise missiles to Mr. Zelenskyy.

Stay frosty, dear readers.

Alternate take:

Regulations and rules and laws indiscriminately targeting everyone doing business, the intent to make illegal or otherwise regulated stuff more difficult to produce, sell et c out of a misguided sense of moral authority, is making legal business even less profitable than the already heavy leavies imposed by taxation and fees - is the "tongue on the scale" causing severly increased rates of bankruptcy.

Two examples from here:

1) Any place serving alcohol outdoors, such as a pub, must from 1 January of this year also have indoor seating, even if the outdoor serving area is a seasonal one, open only during Summer.

Which is causing restauranteurs and pub-owners to shutter their businesses instead of investing lots and lots of money into re-building (after the 1-3 year long waiting time for permits, unless someone appeals the permit-process causing further dealys, add to that tens of thousands, or even higher, fees that must be paid for the process to even start - and paid again in full, every time you re-apply).

2) Selling alcoholic beverages from your own farm or brewery, small-scale, is so tightly regulated it's Pythonesque. One (1) bottle of alcohol, 750ml maximum, 40% maximum, or (3) bottles of wine, or 6L of beer. And to get to buy it, the customer must first sit through a 45 minute seminar arranged by the seller, on the dangers of alcohol consumption.

It's reminiscent of the 1700s, where each kind of fish came with a different tax rate, and taxman, and the fishers couldn't land the fish in Stockholm until the taxman for each kind had done his rounds on all the boats.