Covid in the Eurozone: Disastrous (Economic) Aftermath Indicates Impending Economic Crash

(At least partially) due to Covidistan's insane mandate madness, bankruptcies and inflation are sky-high while energy worries make for a bleak outlook

And here’s the preliminary accounting for the Covid mandate hawks in politics, legacy media, and their fellow travellers elsewhere. As reported by some tabloid outlets—legacy media outlets were, understandably, a bit shy to report on it—bankruptcies and inflation are nowhere as high as they are in Austro-Covidistan.

(Just in case, yes, legacy media brought this story, but if a comparison of the almost literally identical pieces in, e.g., Die Presse and Der Standard is any indicator, they just copy-pasted from the Austrian Press Agency.)

Of course, no-one knows why that is, and even fewer ‘leaders’ are going to claim ‘responsibility’, least of all, I’d bet, the Conservative-in-name-only/Green coalition gov’t.

The below piece appeared in Heute on 11 May 2023; translation, emphases, and bottom lines mine.

Company bankruptcies up sharply: Austria in the lead

Corporate bankruptcies have increased significantly in Europe in 2022. Reason are the high cost of energy and raw materials.

High inflation, energy shortages, and macroeconomic problems have led to a significant increase in corporate insolvencies. Across Western Europe, there were a total of 139,973 insolvencies in 2022. This is more than 24% more than in 2021.

Increase in Austria by almost 60 percent

According to a study by Creditreform, the largest increase in insolvencies occurred in Austria with 59.7%. It was followed by Great Britain (+ 56%), France (+ 50%), and Belgium (+42%). [I wonder where all the ‘Easterners’ are…perhaps drastically ramping up welfare spending wasn’t such a good idea…]

‘Many ailing companies could no longer withstand the multiple burdens’, explained Patrik-Ludwig Hantzsch, Head of Creditreform Economic Research, in a press release.

According to Creditreform, the fact that Austria leads the way in the rise in insolvencies has to do with the Corona regulations and subsidies. In Denmark, Luxembourg, Portugal and Italy, corporate insolvencies actually declined.

Bottom Lines

Austria’s Covid régime was famous for its free for all, no holds barred approach to locking down (most world-wide outside China), testing (at least the most in Western Europe), and the like. Oh, lest I forget, of course subsidies to the population were extremely high.

I recall (can’t find the link right now) that Switzerland handed out, on average, some 100 euros per person until the end of 2022; by comparison, the Austro-Covidian régime paid out in excess of 1,500 euros per person.

Since ‘inflation’ used to mean ‘an increase in the money supply’ (as opposed to the central bankers’ mantra of ‘price stability’), Health and Welfare Minister Johannes Rauch’s recent nightly news appearance in state broadcaster ORF’s popular late-night newscast was telling.

Last week, Mr. Rauch lashed out at retailers and corporations for causing high prices—which would be funny, if Mr. Rauch knew anything about where inflation comes from:

if ‘inflation’ is an indicator of the growth of the money supply, neither retailers nor corporations are to blame

typically, it is a gov’t that, via the central bank, that controls the money supply

but, in the Eurozone, that vital piece of sovereignty was ceded to the European Central Bank (ECB)

Speaking of the ECB—the US Federal Reserve’s poor cousin—here’s a link to their ‘Harmonised Index of Consumer Prices’ (HICP), which features, among others, the following graphs; see if you can spot ‘the pandemic’:

Bonus Feature: The ECB’s Ponzi Scheme Explained

As it happens, there’s more than meets the eye, specifically with respect to the first of the three above-reproduced graphs: what about the money supply?

These data are a bit more tricky to find over at the ECB’s website, but here goes.

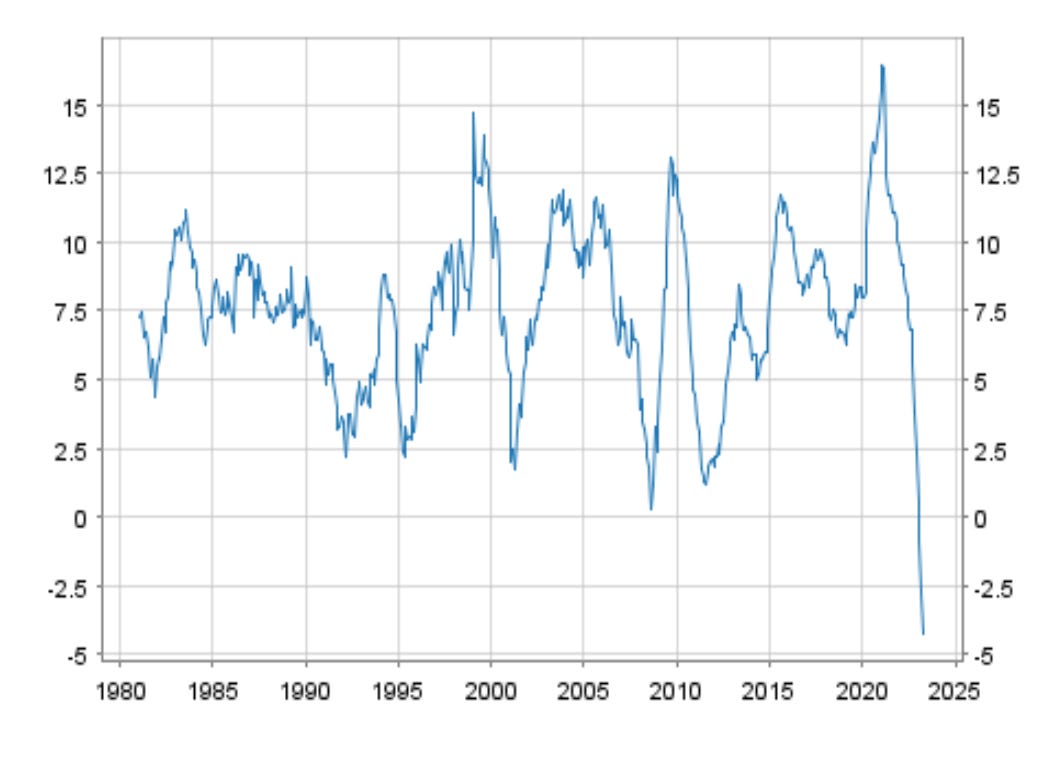

Monetary aggregate (M1) = money in circulation, annual growth rate:

Do note that the data behind the above graph is even more troubling: from March 2020 through November 2022, monthly growth of money in circulation (M1) ranged between 10.1% (Nov. 2022)-10.4 (March 2022) to 16.3-16.4% (Jan., Feb. 2022).

To me, the most absurd notion of the above data, however, is the fact that M1 grew well above 5% every month for the past quarter-century (a quick glance at the data indicates the last time M1 grew by almost nothing was in the depths of the 2008 Great Recession).

Until, well, right now.

In March 2023, there was (provisionally) a -4.2% contraction of the money supply, indicating an acceleration from the the previous months (-2.7% in Feb. 2023, -0.8% in Jan. 2023).

And, yes, this is entirely predictable (see, e.g., my treatments from last August here and here).

The economic bust has almost arrived in legacy media.

It’s going to be a tough summer/autumn, and everything else beyond that point is hard to predict.

Buckling up, though, seems a good idea.

And prepare for disruptions.

Excellent knowledge. Thank you.