BioNTech Reports 700m Losses in 2024

And thus one of the giants of the Covid Mania will likely die: with a whimper, accompanied by the wailing of investors, CEO Ugur Sahin (begging for more taxpayer money), and many broken lives

From the frontiers of investors, we learn that BioNTech, manufacturer of the infamous ‘Pfizer Jab’, posted significant losses in 2024 and announced job cuts.

Translation of non-English content mine, as are emphases and [snark].

Job cuts planned: 700m Euros in losses for BioNTech

BioNTech made billions in profits with its coronavirus vaccine. Following the pandemic, however, the Mainz-based company has recorded a sharp drop in sales. Jobs are now to be cut.

By Stefan Schmelzer, SWR, 10 March 2025 [source]

BioNTech has slipped significantly into the red on its way to developing cancer drugs and now wants to cut jobs. This was announced by the Mainz-based company on Monday.

The reason for the big losses are the high level of investments, particularly in expensive clinical trials. In addition to job cuts, job relocations are also planned. The Mainz headquarters are to be strengthened.

Losses Increase at BioNTech—Turnover Decreases

The bottom line in 2024 was a net loss of around 700m euros. This continues the trend that began when business with the Covid-19 vaccine slowed down [looks like BioNTech is the equivalent of a one-trick pony]. In 2022, profits still totalled around 9.4b euros. By 2023, profit had already shrunk to just around 930m [that’s a drastic decrease by over an order of magnitude; frankly, it’s a (taxpayer-funded) miracle the ‘company’ is still around].

Sales also fell: after 3.8b euros in 2023, it was around 2.75b in 2024 [huhum, what did they sell?]. For the current year [2025], sales are expected to be slightly lower at between 1.7 and 2.2b euros, with continued high expenditure on research and development of 2.6 to 2.8b euros [looks like someone is either be bought by bigger fish or going out of business before too long].

First Cancer Drug to be Launched in 2026

The first marketing authorisation is expected in 2026. According to BioNTech, it is working on the development of mRNA-based cancer therapies [funny how the journo™ left out the terms ‘transfection’ or ‘gene therapy’ here], among other things. Roughly speaking, the aim is to use mRNA to help the patient’s immune system [and how would that work? I mean, modRNA makes the body’s own cells to produce (‘express’) foreign proteins, inducing the immune system to attack these cells: would that cancer drug ‘only’ do that to cancer cells?] Cancer cells could then be recognised and destroyed based on certain characteristics.

Researchers in Mainz are comparatively advanced in the development of preparations for bladder cancer and for the treatment of bowel cancer. Important new study data on the latter is expected at the end of this year or the beginning of next year.

BioNTech Cuts Jobs

BioNTech has now announced job cuts. Over a period of around three years until the end of 2027, there will be 950 to 1,350 fewer employees in Europe and North America [that’s a reduction of employees between 13-19%]. At the end of 2024, BioNTech had around 7,200 employees worldwide.

Due to the lower demand for Covid vaccines, the Marburg site, for example, will be affected, with 250 to 350 of the 670 jobs there to be cut [minus 37-52% jobs]. In Idar-Oberstein, around a third of the 450 full-time positions are to be cut [my best guess is that positions in North America (US) won’t be cut that much].

BioNTech to Expand Mainz Site

In other areas, on the other hand, staff are to be increased, with between 800 and 1,200 jobs being created. Around 350 alone are to be created at the headquarters in Mainz this year. BioNTech speaks of a clear commitment to Germany as a location [well, good riddance, then, I suppose].

Bottom Lies (no pun)

That’s about it for the reporting™ part by state broadcaster SWR. What has happened to induce that kind of reporting™, though, was the publication of Q4 data, incl. the full annual filing with regulatory agencies. You can find that information by simply searching for ‘BioNTech annual report 2024’ or by clicking here.

What SWR won’t tell you are the following snippets of information:

Advanced oncology pipeline including more than 20 active Phase 2 and Phase 3 clinical trials with a strategic focus on two priority pan-tumor programs: next-generation immunomodulator candidate BNT327 and mRNA cancer immunotherapies

Multiple data readouts expected in 2025 and 2026 aimed at providing clinical proof of BioNTech’s pipeline strategy and advancing the Company towards becoming a diversified multi-product oncology portfolio company by 2030

Completed acquisition of Biotheus securing full control of next-generation immunomodulator candidate BNT327, a bispecific antibody targeting PD-L1 and VEGF-A*

Full year 2024 net loss of €0.7 billion and diluted loss per share of €2.77 ($3.00)

Let’s take a brief look, shall we?

So, BioNTech better not lie to regulators (for that would constitute fraud), but simply look at these bullets points one and three: setting aside the generic ‘mRNA cancer immunotherapies’, our one-trick pony BioNTech is banking bigly on BNT327, more about that one in a moment.

For their ‘pipeline’, see here for a listing of products.

So, what about BNT327? Well, they are apparently using it vs. lung cancer (via clinicaltrials.gov), and while there are yet no results reported, I found the following paper in the Annals of Oncology, Volume 35, Supplement 2, S804, September 2024.

Entitled, ‘A phase II safety and efficacy study of PM8002/BNT327 in combination with chemotherapy in patients with EGFR-mutated non-small cell lung cancer (NSCLC)’, we learn the following (in their words):

We present data from an ongoing single-arm Phase II study of PM8002/BNT327 combined with chemotherapy for patients with EGFR-mutated NSCLC who progressed after EGFR-TKI treatment. The correlation between tumor PD-L1 expression and clinical response was investigated.

Please allow me to translate: trial participants received chemotherapy plus BioNTech’s new drug.

Methodology

Patients received PM8002/BNT327 plus carboplatin and pemetrexed Q3W for 4 cycles, followed by maintenance with PM8002/BNT327 and pemetrexed. The primary endpoint is ORR (RECIST v1.1). Analysis by PD-L1 expression was determined by immunohistochemistry (IHC with E1L3N clone; using tumor proportion score (TPS)) in biopsy taken after progression on EGFR-TKI therapy and classified based on TPS as negative (<1%), low expression (1 to 49%), or high expression (≥50%).

What this method does, likely, is that we may never really know if BNT327 ‘works’ (that is, for the patient; for BioNTech, it might anyways).

Results

As of April 12, 2024, 64 patients were tested for PD-L1 TPS: 28 (43.8%) were TPS<1%, 23 (35.9%) were TPS 1-49%, and 13 (20.3%) were TPS ≥50%. All patients were evaluable for safety and efficacy [I’m skipping the numbers and shares here as these were, based on experience with the Covid poison/death juice, all junk anyways]…Any-grade treatment-related adverse events (TRAEs) occurred in 95.3% (61/64) and grade ≥ 3 TRAEs occurred in 54.7% (35/64) patients [do re-read this: 61 of the 64 participants had an ‘any-grade treatment-related adverse events; do keep it in mind]. Any-grade immune-related AEs (irAEs) occurred in 28.1% (18/64) and grade ≥ 3 irAEs occurred in 4.7% (3/64) patients [a third (!) of participants had ‘immune-related’ AEs]. 6 patients discontinued PM8002 and/or chemotherapy administration due to TRAEs with 1 TRAE-related death.

Guess how BioNTech spins this? Well, here goes the conclusion paragraph:

PM8002/BNT327 in combination with chemotherapy showed encouraging antitumor activity and acceptable tolerability profile in EGFR-mutated NSCLC patients that progressed after EGFR-TKI therapy. The anti-tumor activity of PM8002/BNT327 therapy is positively correlated with tumor PD-L1 expression level.

So, this is what the Covid Mania did: we’ve moved the goalposts as to what the terms ‘acceptable’ or ‘tolerable’ mean.

Remember, ‘any-grade treatment-related adverse events (TRAEs) occurred in 95.3% (61/64) and grade ≥ 3 TRAEs occurred in 54.7% (35/64) patients’. This is what BioNTech considers ‘acceptable tolerability’, and we’ve yet to remember that ‘any-grade immune-related AEs (irAEs) occurred in 28.1% (18/64) and grade ≥ 3 irAEs occurred in 4.7% (3/64) patients’.

Yet, this is now somehow ‘acceptable’ (even allowing for lung cancer patients to kinda want to try anything to stay alive).

In the second such trial, BNT327 is used to see with which kind of chemotherapy it works better (I presume), hence we’ll see the same kind of methodological shenanigans we’ve encountered during the Covid Mania: the absence of a placebo control group makes any results, well, essentially meaningless.

Remember all the ‘studies™’ comparing whatever version of the Covid poison/death juices with their next iteration?

It’s this same shit, different smell feeling all over again.

So, we’ll conclude with a few more lines of boilerplate elevator pitches by BioNTech chieftain Ugur Sahin (found in that above-linked press release of his company):

“From the very beginning, BioNTech’s vision has been to translate our science into survival and become an immunotherapy powerhouse. In 2024, we made significant progress towards our vision through important oncology pipeline advancements, including the initiation of global Phase 3 clinical trials for our anti-PD-L1/VEGF-A bispecific antibody candidate BNT327 and key data updates from our mRNA cancer immunotherapy programs,” said Prof. Ugur Sahin, M.D., CEO and Co-Founder of BioNTech. “We expect 2025 to be a data-rich year with multiple important updates from our priority programs, which we believe have disruptive potential and could improve the standard of care, if successfully developed and approved.”

As to the company’s future, well, here’s how BioNTech did in 2024:

Cost of sales were €243.5 million for the three months ended December 31, 2024, compared to €179.1 million for the comparative prior year period. For the year ended December 31, 2024, cost of sales were €541.3 million, compared to €599.8 million for the comparative prior year period. Cost of sales were influenced by COVID-19 vaccine sales and inventory write-downs and scrapping…

Net profit was €259.5 million for the three months ended December 31, 2024, compared to €457.9 million net profit for the comparative prior year period. For the year ended December 31, 2024, net loss was €665.3 million, compared to a net profit of €930.3 million for the comparative prior year period.

For BioNTech’s SEC filings, click here (esp. the F-20 form, 10 March 2025).

For 2025, higher expenses than sales and revenues are anticipated; BioNTech intends to be profitable ‘by 2030’, hence we might consider their financial positions here:

Cash and cash equivalents plus security investments2 as of December 31, 2024, reached €17,359.2 million, comprising of €9,761.9 million in cash and cash equivalents, €6,536.2 million in current security investments and €1,061.1 million in non-current security investments.

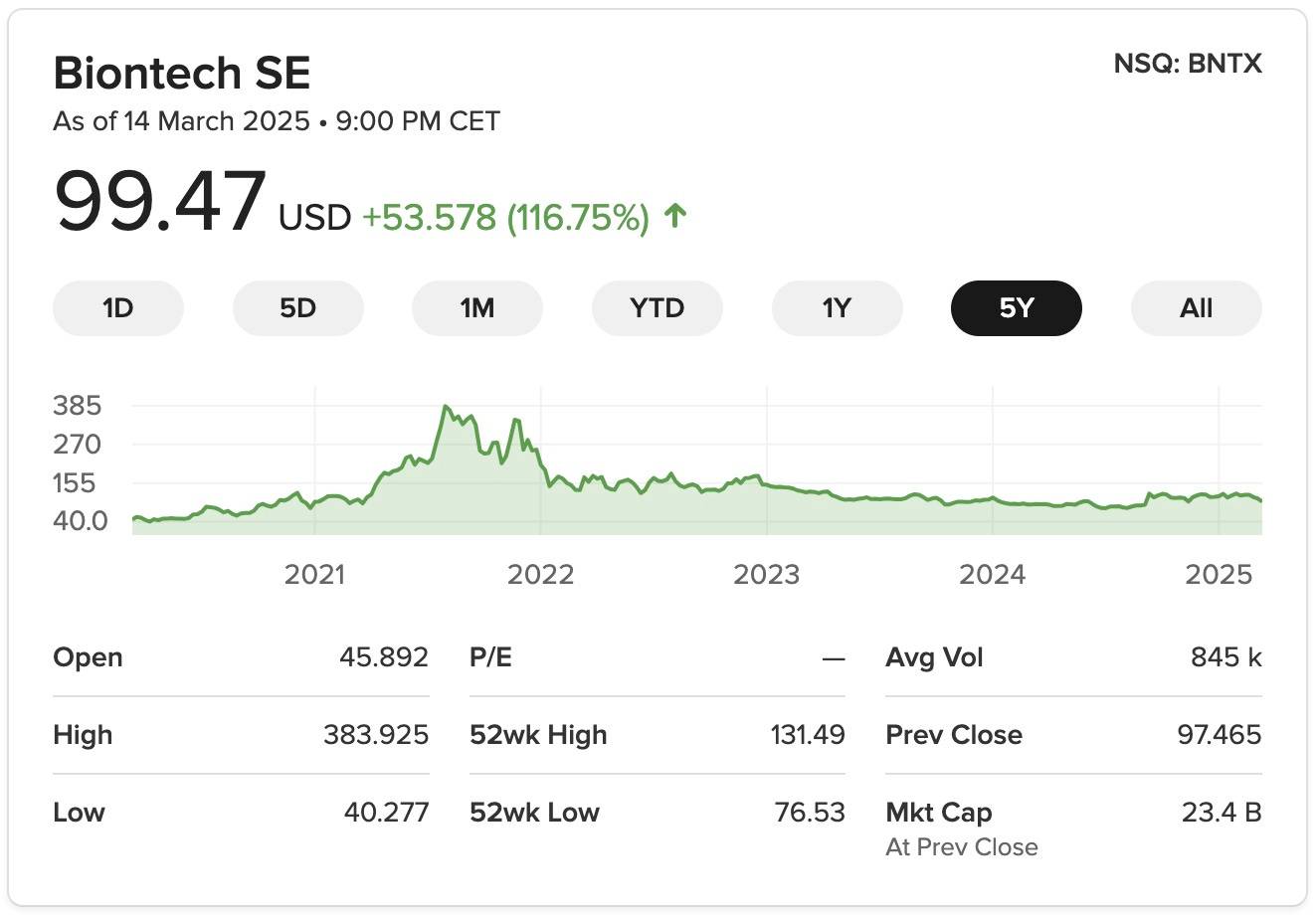

Let’s close this posting by consider their relative share prices:

How much longer do you think they’ll limp along with another 4-5 years to go until profits are anticipated to come in?

Here’s what I think: absent another bout of state-mandated picking of winners—which I don’t consider (lung) cancer treatments to be—and spending insane amounts of taxpayer money, BioNTech (and Moderna) will go away before too long.

I doubt modRNA as a technology platform was ever that useful for large-scale application, and I fully anticipate the next couple of years to bear this out.

Bill Gates visited their HQ in Mainz on the way back from Davos in January, meaning that the company is still of interest. There might be a few more tricks up their sleeves..

Looks like its street address "An der Goldgrube" isn't so auspicious after all ..